I first met Danny Kahneman at a conference on behavioral finance at Harvard University in 1996. I wasn’t struck by his ideas; I was stricken with them. They took me over like an infection; for months, I could think of little else, and for years I pursued more of their implications in the financial world than I could possibly count. In 2001, I wrote a long magazine article about him; in early 2007, we began working on the book that ultimately became Thinking, Fast and Slow. Throughout two years of research, writing, and editing, I tried to keep up with one of the quickest minds, and certainly the most incisive, I’ve ever encountered; it was among the greatest learning experiences of my life. Never before or since has anyone sent me so many worried emails in the middle of the night. No one taught me to question every word I wrote more closely. Nobody ever showed me more profoundly how you can — and should — doubt every belief you passively hold about your world.

Here’s the video of the extensive interview I did with Danny (about 1 hr, 20 min.) for 100 Women in Hedge Funds in 2012:

Know Yourself and Your Decision-Making Process

Here’s a video excerpt of our interview at The Wall Street Journal’s CEO Council in November 2016:

Here’s some of what I’ve written about Danny.

A post for edge.org on what it was like to work with him:

In the nearly two years that I worked with Danny on the book that became Thinking, Fast and Slow, many things amazed me about this man whom I had believed I already knew well: his inexhaustible mental energy, his complete comfort in saying “I don’t know,” his ability to wield a softly spoken “Why?” like the swipe of a giant halberd that could cleave overconfidence with a single blow.

But nothing amazed me more about Danny than his ability to detonate what we had just done.

Anyone who has ever collaborated with him tells a version of this story: You go to sleep feeling that Danny and you had done important and incontestably good work that day. You wake up at a normal human hour, grab breakfast, and open your email. To your consternation, you see a string of emails from Danny, beginning around 2:30 a.m. The subject lines commence in worry (something like “I don’t think this works”), turn darker (“What were we thinking?”), and end around 5 a.m. in a barrage of panic (“This will not do at all”) and despair (“This is just garbage”).*

You send an email asking when he can talk; you assume Danny must be asleep after staying up all night trashing the chapter. Your cellphone rings a few seconds later. “I think I figured out the problem,” says Danny, sounding remarkably chipper. “What do you think of this approach instead?”

The next thing you know, he sends a version so utterly transformed that it is unrecognizable: It begins differently, it ends differently, it incorporates anecdotes and evidence you never would have thought of, it draws on research that you’ve never heard of. If the earlier version was close to gold, this one is hewn out of something like diamond: The raw materials have all changed, but the same ideas are somehow illuminated with a sharper shift of brilliance.

The first time this happened, I was thunderstruck: How did he do that? How could anybody do that? When I asked Danny how he could start again as if we had never written an earlier draft, he said the words I’ve never forgotten: “I have no sunk costs.”

To most people, rewriting is an act of cosmetology: You nip, you tuck, you slather on lipstick. To Danny, rewriting is an act of war: If something needs to be rewritten then it needs to be destroyed. The enemy in that war is yourself.

Having wanted to be a writer since I was 13, I still hadn’t learned how to be one until I worked with Danny. I no longer try to fix what I’ve just written if it doesn’t work. I try to destroy it instead — and start all over as if I had never written a word.

Danny taught me that you can never create something worth reading unless you are committed to the total destruction of everything that isn’t. He taught me to have no sunk costs.

* Here I am paraphrasing, but not by much.

Do You Sabotage Yourself?

By Jason Zweig

When people ask me which investment thinker I’ve learned the most from, they expect names like Warren Buffett, Peter Lynch and John Bogle. But I always give the same answer: Daniel Kahneman. He’s not a great stock picker like Buffett, a masterful fund manager like Lynch or a crusader for investors’ rights like Bogle. Instead, Kahneman is a psychologist at Princeton University who studies how people estimate odds and calculate risks–the very essence of investing. To my mind, Kahneman has done more than anyone else alive to shed light on how to improve our investing judgment and manage risk intelligently.

My fascination with Kahneman began five years ago, when I heard him speak at an investing conference sponsored by Harvard. His blue-green eyes glittering behind heavy eyeglasses, Kahneman swept back and forth like a hungry owl, holding the audience of money managers transfixed. Citing research on everything from American entrepreneurs to Swedish drivers, he explained how prone humans are to “overconfidence,” or the belief that we know more than we really do. He bolstered his case with tales from his own life, confessing that he’d once underestimated by seven years how long it would take to help write a textbook. In an accent that’s part French and part Israeli, he asked, “Do you know how little you know?” Under his keen gaze, those words felt like a challenge to re-examine everything I’d assumed to be true.

As soon as I returned to my office, I hunted down Judgment Under Uncertainty, a hefty anthology of scholarly articles Kahneman had written with his longtime research partner, Amos Tversky (who died that year). I spent the next three days in a fever of intellectual discovery, hiding out in a windowless, soundproof room where no one could interrupt me. Scribbling notes furiously, drawing arrow-strewn diagrams and sprinkling the book with exclamation points, I discovered insights and connections that had long eluded me. Why do people buy high and sell low, when they know they should do the opposite? Why do investors listen to analysts who are clearly clueless? Kahneman and Tversky had the answers.

I felt as if someone had taken the top of my skull off with a can opener and was shining a searchlight inside. What that light revealed was hardly what I’d expected: I was not the rational, sensible investor that I’d always thought I was. In many ways, I now saw, I was a dope. And that, Danny Kahneman has been teaching me ever since, is probably the single smartest thing I–or any investor–could ever figure out.

Others have been similarly enthralled. William Sharpe, the Nobel-prizewinning economist, says the findings of Kahneman and Tversky are “certainly worthy” of a Nobel. “I love their work and always have,” says Sharpe. “There’s a huge amount of information in there that helps us understand how people actually make decisions.”

In this age of instantaneous information, any of us can find out almost everything there is to know about any stock. Why, then, have so many of us lately earned the worst returns of our lives? Because information is useless if we misinterpret it or let emotions warp our judgment. Kahneman’s research throws us a lifeline that can save us from our own self-defeating behavior.

Pigeons, Pilots and IPOs

Kahneman was born in Tel Aviv in 1934, but his French parents returned home to Paris when he was three months old. Six years later, as Kahneman was finishing first grade, the Nazis invaded France, and his family was forced to wear the yellow star that marked Jews for deportation to the death camps. His father, a research chemist, was taken away but then released because he was considered useful to the war effort. The family escaped to unoccupied France and spent the rest of the war in hiding and on the run. His father died in 1944, and 12-year-old Danny moved to Palestine with his mother two years later.

Kahneman thought of becoming a physicist or economist, but he ended up studying math and psychology at Hebrew University in Jerusalem. He finished his B.A. at the age of 20. Having survived so many horrors, he had already developed a deep distrust of things that others take for granted–the notion that humans are rational, the confidence that knowledge can solve all problems, even the belief that there’s a God. He entered the work force as an unorthodox thinker determined to challenge the status quo. In 1955, as a skinny 21-year-old in the Israeli army, he saw that the psychological screening system for recruits was a mess; new soldiers designated as officer material often weren’t, while many of those on combat duty should have been peeling potatoes. Kahneman set out to overhaul the system.

“From the beginning, Danny was different,” says his assistant on that project, Mina Zemach, now Israel’s top political pollster. “He thought like an outsider.” In the 1950s, Israel was a frontier society, and many men wore their shirts unbuttoned. Kahneman insisted on wearing a tie. “If I leave my shirt open,” Zemach recalls him saying, “people will look at my chest when I interview them. I want them to look at my eyes.” After months of interviews, Kahneman replaced the old method of haphazard, subjective questioning with a standardized survey–systematically rating recruits on six factors like aggressiveness and masculine pride. His system was so effective that, with some modifications, the Israeli army used it for decades.

Kahneman went on to earn a Ph.D. at Berkeley, studying statistics, the psychology of visual perception–why things look the way they do–and how people interact in groups. Then, at 27, he returned to Hebrew University to teach statistics and psychology. One former student recalls that Kahneman’s notes for his dazzlingly diverse lectures consisted of a few words scribbled on a cigarette pack on his way to class. “Danny was exhilarating,” says Michael Kubovy, now a psychology professor at the University of Virginia. “He thinks in a way that imports ideas from everywhere.”

Kahneman captured his first great insight by observing his own students. In the late 1960s, he was teaching a class on the psychology of training to flight instructors in the Israeli air force. Concerned at how the instructors screamed obscenities and pummeled trainees’ helmets until they cried, Kahneman told his class that research on pigeons showed reward to be a better motivator than punishment. One flight instructor burst out, “With all due respect, sir, what you’re saying is for the birds.” He heatedly told Kahneman that trainees almost always did worse on their next flight if they’d been praised–and tended to fly better just after getting yelled at.

Kahneman was dumbstruck. He realized he was staring into the face of a profound misperception: The flight instructor believed that his own praise or criticism caused the trainee’s performance to reverse. In reality, Kahneman knew, chance alone dictates that an unusually good or bad event is typically followed by a much more ordinary one–what statisticians call “regression to the mean.”

Regression also explains why hot funds go cold and why the Nasdaq, after doubling in 1998 and 1999, has imploded. But, like the Israeli flight instructor, most investors fail to see how powerful a force regression is. We know in theory that “what goes up must come down”–but, as Kahneman saw that day, we vehemently resist recognizing it in practice.

In 1969, Kahneman asked Amos Tversky, also a Hebrew University psychology professor, to visit his class. Tversky insisted in his lecture that the average person, while flawed, is basically rational in appraising risks and calculating odds. “I just don’t believe it!” exclaimed Kahneman, and after class he and Tversky retreated for lunch. By the time they’d polished off their appetizers, Tversky saw Kahneman’s point–and was raising him. Volleying ideas at each other in an inspired frenzy, they speculated that people use mental shortcuts to estimate probabilities and predict risks. Over the next decade, they ran dozens of experiments that confirmed their lunchtime hypotheses.

- We base long-term decisions on short-term information. The “law of large numbers” holds that only a vast sample of data (a nationwide poll, say) can give an accurate picture of the population it’s drawn from. But Kahneman and Tversky found that the typical person acts on what they christened the “law of small numbers”–basing broad predictions on narrow samples of data. For instance, we buy a fund that’s beaten the market three years in a row, convinced it’s “on a hot streak”–even though a mountain of research shows that three-quarters of all funds underperform in the long run. And many investors concluded in 1999 that growth stocks would clobber value stocks indefinitely, since they’d done so for five–yes, five!–years running. Sure enough, value stocks trounced growth by more than 28 percentage points last year.

- If something is easy to recall, we think it happens more often than it does. Kahneman and Tversky had people listen to a list of male and female names, both famous and obscure, and then recall whether it contained more men or women. When more of the famous names were female, 81% of people concluded that women made up more than half the list–when, in fact, there were more men on the list.

Likewise, it’s easy to recall initial public offerings that have been famously lucrative, like Cisco and Microsoft. Yet IPOs that fizzle–like, say, 3DO Co. or Quarterdeck Software–vastly outnumber those that sizzle. Historically, IPOs have actually underperformed the rest of the stock market by three to five percentage points a year, but many gung-ho investors fail to recognize that the majority of new stocks are stinkers.

- When estimating future values, we “anchor” our projections on any number that happens to be handy. In one experiment, Kahneman and Tversky asked people to estimate various statistics, such as the percentage of African countries in the United Nations. Before each person guessed, the researchers spun a “wheel of fortune” to generate a number between 0 and 100. When the wheel landed on a low number, people tended to guess that African nations made up a small percentage of UN members; when it landed on a high number, they guessed that Africa accounted for much more ofthe UN’s membership.

Experiments like this prove that the mere suggestion of an outside number is enough to distort people’s views. That’s just what happens when an analyst publicizes a price target for a stock. Such targets often are utter garbage–but investors still “anchor” on them. On Dec. 29, 1999, PaineWebber analyst Walter Piecyk slapped a 12-month target of $250 (split-adjusted) on Qualcomm. That day, the stock soared 31% to $165, as investors headed toward Piecyk’s anchor. But 12 months later, Qualcomm had belly flopped to $82, 67% below his target; it now wallows around $50.

The Odd Couple

Pushing ahead with their experiments, Kahneman and Tversky were on fire with what they had found. “Their eyes shone,” says former student Maya Bar-Hillel, now a leading psychologist at Hebrew University. “It was hard to believe that serious work could be so much fun. Danny and Amos never stopped talking about it.”

The two men were like an academic Odd Couple. Tversky was a math wizard with deep, focused knowledge; Kahneman had brilliant instincts and broad interests. Tversky kept nothing on his desk but an expensive pen and one sheet of paper on which he’d scrawl equations from memory, says a former student, while “Danny was always messy and panicked. He constantly couldn’t find things.”

In the late ’70s and early ’80s, they focused on how people perceive risks. Economists had long argued that a rational person will wager an equal amount for the chance to win $100 or avoid a $100 loss. After all, either gamble leaves you $100 better off. But Kahneman and Tversky showed that most people don’t think that way. Try one of their experiments yourself: Imagine a coin toss in which you’d lose $100 if tails came up. How much would you have to win on heads to be willing to take the bet? Most people insist on at least $200. The lesson: Losing $100 feels roughly twice as painful as gaining $100 feels pleasant.

In fact, Kahneman and Tversky concluded that we hate losses so much that we make inconsistent gambles in the hope of avoiding them. Their findings help explain, for example, why people tend to sell their winning stocks too early, while holding on to losers for too long: We want to lock in a sure gain before something jeopardizes it, but we’ll hang on to a losing stock in a bet that it will eventually break into the black.

Kahneman and Tversky’s proofs of the pain of loss also show why more investors don’t stake all their money on stocks. History suggests that stocks should outperform bonds over any period of 30 years–but few of us bet every cent on stocks. That’s because the short-term pain of owning them in a disastrous year like 2000 overwhelms our perception of the long-term gain they should eventually produce.

Kahneman’s Commandments

Today, five years after Tversky’s death, Kahneman is as intense as ever. When I ask him what he plans to do in retirement, he shudders visibly and says, “I don’t want to think about that at all.” The study in his Princeton home is ankle-deep in papers, and he sheepishly admits that he’s never even glanced at the classic English novels his wife buys him.

In the past few years, Kahneman has shifted to measuring what makes us happy. I ask him the obvious: Does money buy happiness? “Not exactly,” he says. Even as wealth has surged in recent decades, the percentage of Americans who say they’re happy with their lives has remained basically the same. But money does buy happiness in one sense, Kahneman notes. The key is not how much you have, but how you spend it. “There’s good evidence,” he says, “that people get more pleasure from things they’re not habituated to.” Like what? “Flowers, feasts, vacations,” he offers. “Try to spend your money on things you won’t get used to or tired of.”

As the ultimate authority on why most of us fail to get rich, Kahneman would seem ideally equipped to master the stock market. But when it comes to investing, he says, “I don’t try to be clever at all.” He largely sticks with index funds, which buy and hold a vast array of stocks. Comfortable with his limitations, he doesn’t chase individual stocks or trade in and out of the market. “The idea that I could see what no one else can is an illusion,” he says.

Few of us are as honest about our shortcomings as Kahneman is. Yet we can all benefit from applying his insights to our portfolios. Here are the lessons I’ve learned from him.

- Distrust data. Rather than leaping to conclusions based on scant data, look at as many numbers as possible. Don’t rely just on recent performance; look at several time periods. “It doesn’t take many observations to think you’ve spotted a trend,” warns Kahneman, “and it’s probably not a trend at all.” Merrill Lynch, for instance, recently told investors to slash their exposure to overseas stocks since foreign returns have lately resembled those of U.S stocks. But what if that proves to be an aberration?

- Chill out. The hotter an investment’s recent returns are, the more skeptical you should be about its future. Remember to ask what eventually became of other similarly faddish investments. Until lately, years of easy profits had made investors much too confident. As Kahneman wryly notes: “In a rising market, enough of your bad ideas will pay off so that you’ll never learn that you should have fewer ideas.”

- Anchors aweigh. When pundits like Goldman Sachs’ Abby Joseph Cohen predict where the Dow is heading, or when analysts like Morgan Stanley’s Mary Meeker forecast Amazon.com’s stock price, the market often moves magnetically in their direction. But don’t anchor your expectations to the tea leaves of the so-called experts. At best, they’re making educated guesses; at worst, they’re manipulating you to make money for their own companies.

- Use mad money. If you can’t resist the temptation to trade stocks, put the bulk of your portfolio in a broad stock-index fund; then take a little (10% tops) to “play the market” yourself. This way, you keep your hunches on the fringe, where they belong. “It’s like going to the casino with only $200,” says Kahneman. “It helps protect you from regret.”

- Step back. In scary times like these, force yourself to look at your whole portfolio. Last year, my stake in AOL Time Warner (MONEY’s parent) plunged 57% in the fourth quarter. But Kahneman has taught me to use what he calls “global framing,” or looking at the sum total of everything I own. It turns out my entire portfolio was down only 8% that quarter and was flat for the year. So I didn’t sell, because I didn’t panic–and my 57% loser has since bounced back.

- Stop counting. “If owning stocks is a long-term project for you,” says Kahneman, “following their changes constantly is a very, very bad idea. It’s the worst possible thing you can do, because people are so sensitive to short-term losses. If you count your money every day, you’ll be miserable.” So I check the value of my investments a grand total of four times a year; while others agonize over what their stocks did from 1:24 p.m. to 1:37 p.m. today, I’m more concerned about where mine will be between the years 2024 and 2037.

- Fly on autopilot. Many of the people who loved the Nasdaq when it was at 5000 a year ago won’t touch it now that it’s at less than half that level. Such irrational mood swings lead people to trade too much as they veer erratically between glee and dismay. “All of us,” says Kahneman, “would be better investors if we just made fewer decisions.”

Luckily, there’s a solution called dollar-cost averaging. Every month, an automatic electronic transfer sweeps money out of my bank account and into index funds. I never try to predict where the market is going; I just mechanically shovel more cash into my funds each month, regardless of whether the market has been going up, down or sideways. I call this my “permanent autopilot portfolio.” It gets me out of trying to guess what will happen next–a game that Kahneman has taught me I can’t win.

- Look within. Most financial advice, especially on TV and the Internet, suggests that investing is an endless race to beat the market. Every day brings a breathless stream of bulletins about who’s ahead or behind. If anyone else wins, it seems, you lose. But Kahneman’s insights teach us something very different and vastly more profound: Investing isn’t about beating others at their game. It’s about controlling yourself at your own game. I’m not a penny poorer if someone in Dubuque beats the S&P 500 and I don’t. But I can ruin my family’s financial future if I lose my self-control and let my greed or fear trick me into buying high or selling low.

For each of us, risk doesn’t reside only in the market. It lurks inside ourselves–in the way we misinterpret information, fool ourselves into thinking we know more than we do or overreact to the market’s swings. By teaching me the paradox that the most powerful thing I can learn is how little I can ever possibly know, Danny Kahneman has set me free.

If you like, here are PDFs of that profile, along with one of a Q&A I did with him while we were working on Thinking, Fast and Slow. These color PDFs are large files and may take a while to load; you might need to right-click, Ctrl+click, or hold down your cursor.

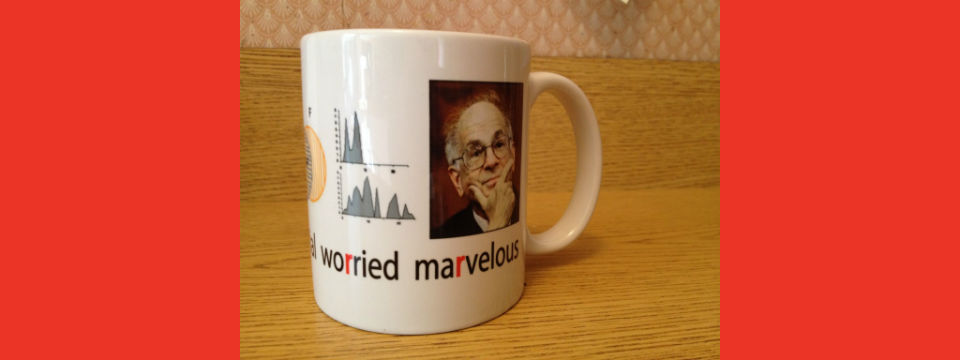

A brief note: The coffee mug at the top of this post was a party favor from “Dannyfest,” a celebration of his work held in New York in May 2008. The letter R is highlighted in red to commemorate classic research he did with Amos Tversky showing that people tend to believe that words beginning with the letter R are more common than words in which R is the third letter — even though R is more common in the third position. (Or should I say “moRe” common?)

Read the rest of the column

This article was originally published on The Wall Street Journal.

Further reading

Daniel Kahneman, “Maps of Bounded Rationality” (Nobel lecture, video and transcript); text-only version here

Amos Tversky and Daniel Kahneman, “Judgment under Uncertainty: Heuristics and Biases,” Science, 1974

Daniel Kahneman and Amos Tversky, “Prospect Theory: An Analysis of Decision Under Risk,” Econometrica, 1979

Amos Tversky and Daniel Kahneman, “The Framing of Decisions and the Psychology of Choice,” Science, 1981

Michael Lewis, The Undoing Project: A Friendship That Changed Our Minds

What I Learned from Daniel Kahneman

When the Stock Market Plunges…Will You Be Brave or Will You Cave?

Behavioral Finance: What Good Is It, Anyway?