Perhaps the least appreciated aspect of the rise of passive fund management and the decline of active is how shamelessly the active-management industry has contributed to its own collapse. Index funds would never have been able to become such an existential threat if stock pickers had run their own businesses more thoughtfully. I highlighted the shortcomings of the active-management business almost eighteen years ago in this guest essay I wrote for the great economist and investment consultant Peter Bernstein‘s newsletter. The response, at the time, was an outpouring of agreement from senior executives throughout the asset-management business — none of whom, so far as I could ever tell, did a thing about the problems they said I had diagnosed so clearly. Quite the opposite: Many of them went on to commit the same strategic blunders with more enthusiasm than ever.

A few excerpts:

Here, then, is one of the harshest truths of the information age: Cash flow from clients now rivals the investment process itself as the main determinant of total return. Thousands of retail investors, each wielding only a few thousand dollars, can smother a fund manager with cash as soon as they detect what appears to be outperformance. Alpha has always been perishable, but in today’s world of instantaneous information it is likely to have the shelf life of unrefrigerated fish. When a fund manager goes from absorbing a trickle of cash flow, to drinking from a fire hose, to surfing a tsunami, his past performance loses all relevance.

The time has come for investment managers to concede that, beyond a certain rate, asset growth is indistinguishable from suicide.

If he wants to excel, a manager must ignore tracking error and shatter the stylistic chains the middlemen want to shackle him in. But if he scoffs at tracking error in his quest for higher long-term returns, then he runs a much greater risk, at least in the short term, of underperforming somebody’s benchmark.

Since prevailing opinion is priced so rapidly into each popular stock as a form of public information, why go to the expense of forming your own opinion by gathering your own private information? It’s well-documented that birds behave this way, but now we are witnessing the sad spectacle of the smartest people in the world doing the same thing. When most information can no longer earn back the cost of gathering it, herding becomes the best short-cut to relative success.

Thus in today’s environment, in matters not one whit whether the market is efficient or not. If the tidal wave of short-term information has obliterated long-term thinking by managers and clients alike, if most managers are far too sheepish to capture any inefficiencies, and if they refuse to modulate the monstrous cash flows from their clients, then there can be no salvation for active management in the aggregate. Instead, managers must show the courage to shatter the system from within…. Otherwise, active management will remain what it has so sadly become: a deep out-of-the-money call option on hope — with no exercise date.

A PDF is here: plbjz-copy; please do not circulate without crediting www.jasonzweig.com.

A transcript follows below, with a few links, footnotes, and paragraph breaks added for clarification and easier reading online.

The Velocity of Learning and the Future of Active Management

Now here, you see, it takes all the running you can do to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!

The Queen in Lewis Carroll’s Through the Looking Glass

For most of human history, the desire for knowledge and its ultimate arrival were separated by huge gulfs of space and time. After the Children’s Crusade set out from Marseilles in the year 1212 to help drive the Muslims out of Jerusalem, fully 18 years passed before news of the children’s fate (mainly enslavement and death in North Africa) made its way back to Europe. And the first news of the Boston Tea Party did not reach London until Jan. 19, 1774 — a full month after Samuel Adams and his rabble of patriots raided three British merchant ships and dumped their shattered cargo into Boston harbor.

No wonder the early securities markets sprang up around coffee shops near the water’s edge, where heavily caffeinated brokers could pounce on the news as soon as ships nudged against the docks. In 1790, speculators cashed in on Alexander Hamilton’s proposal to restructure the Federal debt by hiring sleek ships to outrace the spread of the news on land, enabling them to buy U.S. paper for as little as 20 cents on the dollar; they doubled their money in days. Early in the 19th century, Nathan Mayer Rothschild built a fortune arbitraging foreign bonds and currencies as his carrier pigeons and couriers slipped him the earliest news from Europe.[modern_footnote]Some historians argue that this oft-told anecdote should apply, instead, to the economist and bond speculator David Ricardo.[/modern_footnote] In those days, too, information was a precious and tangible asset whose first owner could extract all the value for himself.

Today, however, information moves everywhere at once, and the future has collapsed like a spent accordion. More than 105,000 Bloomberg terminals around the world flicker with a little green “up” arrow a few milliseconds after an uptick in any security, and each analyst’s earnings forecast, no matter how bold or thorough, disappears with barely a splash into the rushing river of consensus forecasts. The investor relations department’s “earnings guidance” has long since been supplanted by whisper numbers, which in turn have been superseded by “pre-whispers.” We are so inundated with information that we “know” the future now; only this moment matters, and action is everything. In 1959, the average mutual fund’s turnover rate was 16.4%, equating to a six-year holding period; by 1979, it was 63.3%; and now it has passed 83%, or just 14 months of ownership. How bad can it get? A recent study found that day trading is most profitable for time horizons shorter than one minute and 20 seconds; after five minutes, the mean profit disappears entirely.

Why should we care if the velocity of learning has reached warp speed? The proverb “A bird in the hand is worth two in the bush” appears to have universal force across the species that behavioral ecologists have studied; animals ranging from bumblebees to elephant shrews discount the value of delayed rewards along a hyperbolic curve that is steepest in the near-term future. Humans, it turns out, are no different.[modern_footnote]With hindsight, this strikes me as an overstatement. While humans do discount the future steeply, we are significantly more patient than other species.[/modern_footnote] Look at the graph below. The vertical bars represent the absolute value of potential rewards; the curves plot how the subjective value of those rewards change as the time to receive them approaches. When time horizons are long (in the region of t2), the larger, more remote risk is more attractive. But when delays are shorter (in the region of t1) then the smaller, closer risk becomes far more preferable. (Simply put, when we’re hungry, we would rather eat a smaller meal right away than a larger one later.) As today’s flood of data makes the future seem closer and more knowable, investment managers are shoved eastward along the x axis, into the zone where long-term gambles become much less attractive than they used to be.

Now ask yourself: In this context, what purpose does more information serve for me and my clients? Richard Dawkins, the distinguished professor of evolutionary biology at Oxford, had this to say in a recent interview with the BBC:

“Aristotle was an encyclopedic polymath…. Yet not only can you know more than [he did] about the world. You can also have a deeper understanding of how everything works. Such is the privilege of living after Newton, Darwin, Einstein, Planck, Watson, Crick and their colleagues. I’m not saying you’re more intelligent than Aristotle, or wiser…. That’s not the point. The point is only that science is cumulative, and we live later.”

Dawkins is echoing Sir Isaac Newton’s remark that “if I have seen further it is by standing on the shoulders of Giants.” But in money management, the cumulative advance of knowledge does not simplify the lives of those who come later. It makes their jobs harder. Warren Buffett is a giant, and you can stand on his shoulders all you like, but your are unlikely to see further — because what he sees has long since been telegraphed to every one of your competitors. As Hayek pointed out decades ago, “The ‘data’ from which the economic calculus starts are never for the whole society ‘given’ to a single mind which could work out the implications, and can never be so given.”

Meanwhile, individuals have joined institutions in thrall of instantaneous learning. A sanitation worker in Des Moines, updated non-stop by CNBC and the internet and armed with toll-free telephone numbers and a computer mouse, can engage in instantaneous performance arbitrage at no frictional cost. Through “mutual-fund supermarkets” like those run by Charles Schwab, Fidelity, and Waterhouse, retail investors and financial planners can pile-drive hundreds of millions of dollars into (or out of) a fund in a matter of weeks.

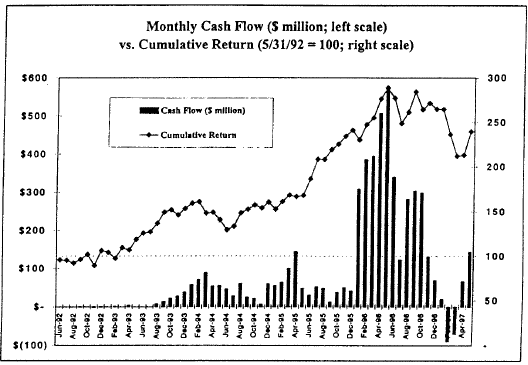

The chart above depicts the relationship between performance and cash flow at a leading small-company mutual fund over the five years ending May 31, 1997. As you can see, while the value of the portfolio was rising rapidly from mid-1992 through early 1994, almost no one was investing in it. Then, at the end of 1995, this became the no. 1-ranked capital-appreciation fund for the trailing three, five, and ten years — and the manager yodeled out its rankings in print ads across the land. In the next six months, the fund (which at the end of 1992 had total assets of only $3 million!) took in $2.5 billion in new cash from frenzied investors. Then Murphy’s law of cash flows kicked in: Just as money cascaded in, the value of small stocks went down the drain. And this fund could no longer trade its small stocks in small blocks; it had to dump them en masse into a panic.

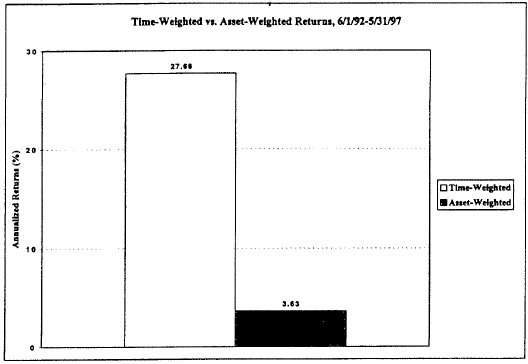

The end result, shown in the chart below: Only a tiny minority of shareholders earned returns remotely resembling the giant gains that the portfolio generated. Many of them captured only losses. Compare the portfolio’s time-weighted return — a stunning 27.68% compounded annually for five years — with its asset-weighted return, which shows how the average dollar invested in the fund fared. While the portfolio outperformed the S&P 500 by a factor of 1.5 to one, its typical shareholder earned only 3.63% annually, or about half the return on a bank CD. As a coda, I must note that this fund’s assets — which peaked at $6 billion in late 1996 — now stand at just $3.4 billion. Performance, meanwhile, has gone from the top decile to the tenth. The public giveth, and the public taketh away.

Here, then, is one of the harshest truths of the information age: Cash flow from clients now rivals the investment process itself as the main determinant of total return. Thousands of retail investors, each wielding only a few thousand dollars, can smother a fund manager with cash as soon as they detect what appears to be outperformance. Alpha has always been perishable, but in today’s world of instantaneous information it is likely to have the shelf life of unrefrigerated fish.

When a fund manager goes from absorbing a trickle of cash flow, to drinking from a fire hose, to surfing a tsunami, his past performance loses all relevance. “The more successful I was,” George Soros has recalled, “the more I was punished by having more money to run.” While illiquidity is the ally of the small, entrepreneurial investor, it is the mortal foe of the giant investment firm. The market may sometimes leave $20 bills lying on sidewalks — but not the best-lit sidewalks with the most pedestrian traffic.

A manager accustomed to running a few hundred million dollars can daintily pluck up the occasional $20 bill in the market’s side alleys; but once he has battened on billions of dollars of new cash, his own girth will limit him to liquid stocks that can hold giant sums without bursting.

If cash pours in as the market is rising, the manager will suddenly be far less than fully invested, through no fault of his own — and doomed to underperform under the dead weight of cash.

If cash pours out in the midst of a drop in stocks, the manager becomes a forced seller.

Even if the cash comes in with a steady gush, it will bloat the manager’s trading costs in the best of markets. In the evocative words of Ted Aronson of Aronson + Partners, “If transaction costs are fire, assets are kerosene.”

The time has come for investment managers to concede that, beyond a certain rate, asset growth is indistinguishable from suicide. In his classic On Growth and Form, the great British morphologist D’Arcy Wentworth Thompson showed that trees quite literally cannot grow to the sky, lest they either keel over or be crushed under their own weight. In fact, no organism can forever grow unconstrained: “there comes a time when…the active and creative energies of growth pass the bounds of physical and physiological equilibrium: and so reach the limits which…natural law has set between what may and what may not be.”

The cult of instant information distorts investment management in another way: Over the past decade, the performance-measurement industry has come out of nowhere to wield immense power. Frank Russell Co., the largest pension consultant, helps sponsors decide on the disposition of $561 billion; even the 20th-largest consultant, Milliman & Robertson Inc., helps allocate $74 billion in sponsors’ assets. Financial planners control at least $75 billion in mutual funds, and brokerage “wrap accounts” hold $80 billion more. All told, this middleman industry holds sway over several trillion dollars in assets — perhaps as much as one-third of the total U.S. stock market by value.

Unfortunately, even as the market has become more informationally efficient over the past 30 years, our statistical tools for distinguishing skillful managers from lucky ones have remained blunt instruments.[modern_footnote]In 2017, I find the sentence that I wrote in 1999 to be incoherent. I think what I meant was: “Our statistical tools for distinguishing skillful managers from lucky ones still tell the same story they did decades earlier.”[/modern_footnote] Michael Jensen’s “The Performance of Mutual Funds in the Period 1945-1964,” published in the Journal of Finance in 1968, reads as if it had been published last week. We still cannot prove that skill exists; all we can prove is that its existence cannot be disproven.

So the middleman industry has little choice but to measure the things that can be measured with high degrees of certainty — and it no longer measures them merely annually or quarterly, but daily. That, in turn, has helped raise relative performance to absolute importance. You can’t eat relative returns, but after 16 years of a bull market, no one even cares what absolute returns taste like. The performance intermediaries want to control tracking error; that’s their risk, because it can be measured so precisely, and it has become money managers’ prevailing definition of risk as well.

“Style purity” — the notion that a manager must forever hew to the straight-and-narrow of a specific “discipline” — is another new orthodoxy driven by the specious premise that performance can be forecast with precision. Managers are commonly arrayed in quadrants determined by value and size factors — for example, small-cap growth or large-cap value. Their deviation from these style boxes is now measured in basis points.

Now I ask you: Into which style box shall we place Warren Buffett? Most observers would like to call Buffett a large-cap value manager. Yet many of his holdings, like Flight Safety and International Dairy Queen, are not large; his biggest, Coca-Cola, is not “value.” Likewise, into which pigeonhole shall we place Sir John Templeton or Peter Lynch? Can anyone say, or should anyone in his right mind care, by how many basis points these giants strayed from their “designated” styles?

That brings us to the core of a killing paradox: If he wants to excel, a manager must ignore tracking error and shatter the stylistic chains the middlemen want to shackle him in. But if he scoffs at tracking error in his quest for higher long-term returns, then he runs a much greater risk, at least in the short term, of underperforming somebody’s benchmark. Scarier still, he is likely to raise the standard deviation of his returns, making it even harder than it already is for the middlemen to establish that he is skillful, not lucky. Thus, liberation from tracking error is worse than heterodoxy; it is heresy.

Once your goal is to minimize tracking error, you are stuck buying stocks where you have the thinnest informational edge. Since prevailing opinion is priced so rapidly into each popular stock as a form of public information, why go to the expense of forming your own opinion by gathering your own private information? It’s well-documented that birds behave this way, but now we are witnessing the sad spectacle of some of the smartest people in the world doing the same thing. When most information can no longer even earn back the cost of gathering it, herding becomes the best short-cut to relative success.

Thus, in today’s environment, it matters not one whit whether the market is efficient or not. If the tidal wave of short-term information has obliterated long-term thinking by managers and clients alike, if most managers are far too sheepish to capture inefficiencies, and if they refuse to modulate the monstrous cash flows from their clients, then there can be no salvation for active management in the aggregate. Instead, managers must show the courage to shatter the system from within. Rather than trying to achieve the lowest tracking error and the highest time-weighted relative returns for their portfolios, firms should focus on producing the highest rate of asset-weighted returns for their clients — by bitterly fighting short-term behavior and the shuffle of the herd, by resisting the G-force of cash flow before it crushes alpha, by setting asset ceilings for their most sensitive funds, and by investing massively in educating their clients. Otherwise, active management will remain what it has so sadly become: a deep out-of-the-money call option on hope — with no exercise date.

Further Reading

Peter L. Bernstein, Capital Ideas: The Improbable Origins of Modern Wall Street

Jason Zweig, Your Money and Your Brain

Jason Zweig, The Devil’s Financial Dictionary

Benjamin Graham, The Intelligent Investor

Dimitri Vayanos and Paul Woolley, “An Institutional Theory of Momentum and Reversal” (non-technical summary here)

Source: Guest essay for Peter L. Bernstein’s “Economics and Portfolio Strategy,” Feb. 1, 1999

Source: Economics and Portfolio Strategy (Peter L. Bernstein, Inc.), Feb. 1, 1999