Here, from my archives, is one of the many articles I’ve written on calibrating your expectations — usually downward. It still has lessons for today, I think. As G.K. Chesterton wrote so wisely, “Blessed is he who expecteth nothing, for he shall enjoy everything.”

A Matter of Expectations

Money Magazine, January 2001

How much will stocks return in the future?

Few questions are more important to investors — and few are harder to answer.

What proportion of your money you put into stocks and how prosperous a retirement you have hinge on how much you expect stocks to return over time and whether the future lives up to your expectations.

These days, as recent surveys of individual investors by Scudder Kemper and PaineWebber show, most people seem to expect the stock market to return about 12% to 15% a year over time. Based on history, that sounds plausible enough. Since 1926, according to the keepers of stock market research at Ibbotson Associates in Chicago, large U.S. stocks have gained 11.2% a year, on average. And according to data from Jeremy Siegel, a finance professor at the Wharton School who has tracked stock returns all the way back to the Jefferson Administration, U.S. stocks have averaged nearly a 9%-a-year return since 1802.

How can we tell if expectations like these are reasonable?

Misusing the past

Unfortunately, 75 years — even two centuries — of data don’t prove that stocks will average at least a 10% annual gain in the future. That’s because the past is not merely that portion of the future that has already happened. Au contraire; if the present is drastically different from the past, warns Yale economics professor Robert Shiller, then “history cannot be a reliable guide to the future.” In the past, the stocks in Standard & Poor’s 500-stock index sold for an average price of 25 times their dividend income and 15 times their net profits — meaning that investors back then got to buy at bargain prices. But now, even after last year’s sell-off, the S&P 500 sells at 86 times dividend income and 26 times earnings — about as expensive as U.S. stocks have ever been. Common sense says that you’re not likely to get high future earnings out of anything if you pay too high a price for it.

Still, many pundits claim that stocks will always outperform bonds because equity investing gives you a piece of a growing business, while bonds simply allow you to lend money at a fixed rate of interest. But what if the rate of interest on bonds is at least as high as the expected growth of the businesses? Then bonds could beat stocks for surprisingly long periods, as they did for the 20 years that ended in 1948 and again for the 17 years that ended in 1982.

Some of the smartest investment thinkers I know of, such as Yale’s Shiller, Robert Arnott of pension fund manager First Quadrant in Pasadena and institutional investor Jeremy Grantham of Grantham Mayo Van Otterloo & Co. in Boston, believe we may be at the start of another period in which stocks will lag bonds — and may even lose money — for years.

Measuring the future

Before you panic, it’s worth learning how the pros put their forecasts together. I spoke with Grantham; John Bogle, the founder of the Vanguard funds; and Laurence Siegel, director of investment policy research at the Ford Foundation. Their forecasts of average annual returns over the next decade or so range from Grantham’s -2% to Bogle’s (and Laurence Siegel’s) 6% to 9%. They all agree that future returns depend on two factors. The first is the growth of corporate profits and dividends (including the repurchase of shares by the companies that issued them). Bogle calls these combined elements “the investment return.” All these experts agree that the long-term investment return should reliably average between 5% and 6% annually before inflation.

The second factor, which Bogle calls “the speculative return,” is the change in market valuation over time — a huge wild card. As investors become willing to pay more (or less) for stocks in the future than they are today, the market’s price/earnings ratio will go up or down, raising or lowering future stock returns accordingly.

Unfortunately, no one has a clue how to read the mood rings of tomorrow’s investors. Jokes Laurence Siegel: “I decided not to put that in my forecast because I’m scared to.” Bogle warns: “The speculative element is as unpredictable as the investment return is predictable.”

But Grantham is willing to guess how investors’ sentiment will change. He reckons that the S&P 500 will go from selling at 26 times earnings today to 17.5 a decade from now — “a friendly, optimistic assumption,” he says, since it’s above the long-term average P/E of less than 15. That single adjustment accounts for most of his forecast that stocks will lose nearly 2% a year after inflation for the next decade.

As the old saying goes, there are two kinds of forecasters: those who are wrong and those who know they are wrong. So you’ve got to take all these predictions about future stock returns with a grain of salt the size of Mount McKinley. However, while they may not be right, these forecasts aren’t useless. Here’s how they can help you think about your own future returns.

Hope for the best, but expect the worst. You won’t suffer if stocks do better than you expected, but if they do worse, your dreams could be demolished. And the higher your expectations, the lower your chances of having them fulfilled.

Do you think stocks will return, say, 25% a year in the future? Despite the 21% average returns of the past five years, a 25% long-run return is about as likely as a Pat Buchanan pep rally in Palm Beach. According to the researchers at Sanford C. Bernstein & Co., over the past half century only 10% of companies in the S&P 500 have increased their earnings at an average rate of at least 20% a year for five years running. Only 3% have raised earnings at least 20% annually for a decade. And none — zero, zippo, the big schneid — have sustained 20% earnings growth for 15 years or more.

In the long run, it’s just not possible for stocks to go up faster than the earnings of the companies they represent; the past few years’ average returns of better than 20% cannot last. Be realistic, and scale back your expectations. As G.K. Chesterton said, “Blessed is he who expecteth nothing, for he shall enjoy everything.”

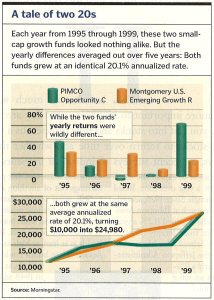

What’s average? The stock market is not a bank CD; when you hear that stocks have returned an “average” of 11% a year, that doesn’t mean they gained 11% every year. In fact, in all the years since 1926, stocks have returned 11% only one solitary time (in 1968), and they’ve gained between 10% and 12% in only three of those 75 years. The rest of the time, returns were all over the place, from a 43.3% loss in 1931 and a 26.5% drop in 1974 to a 52.6% gain in 1954 and a 54% surge in 1933. As you can see from the graphs at left, the same average rate of return can be earned in astoundingly different ways. That’s just how investment math works.

It’s not surprising for a short-term result to differ from what you expect for the long run; in fact, it’s normal. So brace yourself for surprises. And remember that a bad year like 2000, or even several sorry years, can’t tell you anything about what you’ll earn in the long run.

Bad news, good news. What if the bears do turn out to be right? If you’ve complemented your U.S. stocks with bonds, foreign stocks and, perhaps, specialized investments like real estate investment trusts, you’ll always have something that goes up. But the best thing about a protracted down market is that stocks will go on sale, and stay on sale, for years.

Unless you’re retired, that may turn out to be the best investment news of your lifetime. Wall Street hasn’t put stocks on the remainder rack since 1973-74, when the market lost roughly 40% and P/E ratios fell to half their long-term averages. If it takes you by surprise, a sudden sale is a disaster. But if you’re prepared, you can shop while stocks drop, and muster the years of patience it could take for them to recover. Personally, I say, “Bring it on.”

Source: Money Magazine, January 2001

Read the rest of the column

This article was originally published on The Wall Street Journal.

Further reading

John C. Bogle, Thinking About What Lies Ahead for Investors

Michael J. Mauboussin et al., The Base Rate Book: Integrating the Past to Better Anticipate the Future

Definitions of EXPECTED RETURN, SURVIVORSHIP BIAS and THE PAST in The Devil’s Financial Dictionary

Chapter Four, “Prediction,” in Your Money and Your Brain