I recently spoke with April Rudin about my book, The Devil’s Financial Dictionary, for the Huffington Post. Here’s a transcript, with snippets from the text of the book dropped in.

1. The Devil’s Financial Dictionary is a refreshing mix of tongue-in-cheek humor and education. Is this book more about entertainment, or can investors use the information in the book to generate better returns?

Both, I hope. I think if if you can make people laugh, you can help them learn. I hope the book is entertaining and enlightening at the same time. If economics is the dismal science, then investing is the abysmal art — or so, at least, most books on the topic make it seem. I wanted to bring some fun and mischief and irreverence to it, to demystify it, to take the boredom out of it.

2. In your book, you describe alpha, which is the ever-elusive metric that all traders are constantly hunting, as “luck.” Does that mean that you believe there is no such thing as good and bad stock pickers, only lucky and unlucky ones?

I have no doubt that skill exists. But identifying a stock-picker who is skillful rather than just lucky is at least as hard as stock-picking itself. Because so many portfolio managers are highly intelligent, well-trained and diligent, the main factor that distinguishes one from another is luck — just as, in professional sports, the outcome of a game between teams of elite athletes so often turns on a single bad bounce of the ball, a questionable referee’s call, an injury or an error.

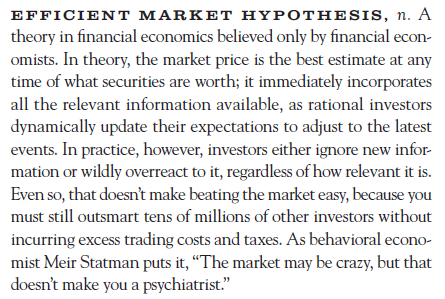

3. In your definition for the Efficient Market Hypothesis, you say that investors “either ignore new information or wildly overreact to it.” Do you believe that there are traders out there that can consistently recognize this apathy/overreaction and profit off of it?

That kind of mispricing often doesn’t last very long:

4. In your book, you quote Meir Statman’s quip, “The market may be crazy, but that doesn’t make you a psychiatrist.” Not everyone is a psychiatrist, but some people are. Is there such a thing as a “market psychiatrist,” and are they better stock pickers than the rest of us?

To some extent, yes. Warren Buffett and his business partner, Charlie Munger, have shown over many years that they are adept at reading other people’s moods, particularly when investors coalesce into a crowd that is either euphoric from rising prices or miserable from falling prices. Benjamin Graham, Buffett’s teacher, seems to have had the same knack. Taking the other side of the emotional trade from the crowd can certainly be profitable, but I’m not sure there are simple, reliable signposts that any of us can use to determine when mob psychology has gotten out of hand. We should be skeptical of whether more than a few geniuses have a knack for it.

5. Should an investor understand every holding in every fund in his or her 401(k)?

No, but you should know why you own what you own, what the funds are seeking to accomplish and how much they charge. You should make sure there isn’t a cheaper alternative available. And you should have general expectations for the rates of return that your holdings are likely to provide — based on decades of history, adjusted slightly for whether the prevailing mood among investors is optimism or pessimism.

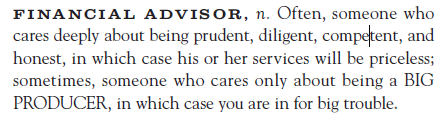

6. Does the world need financial advisors?

The world hugely needs financial advisors. But let’s contrast two definitions from The Devil’s Financial Dictionary:

7. What role should financial advisors serve in their clients’ lives?

A good financial advisor should be like anyone else who provides good advice: a voice of reason and sound judgment that emanates from experience and expertise — not a clown dispensing “tactical” claptrap and pretending to be able to beat the market. We will know the industry has become a profession when financial advisors have to document their returns just as mutual funds and other investment managers do. Until that day comes, they should stop making unsubstantiated claims about their portfolio-management “skills” and should focus instead on the financial planning – retirement, taxes, debt management, estate planning, etc. — that is the greatest benefit a good advisor can provide.

8. Is Wall Street’s use of complicated jargon to sell their products and services more self-serving and manipulative than most other industries that use the same technique?

Wall Street has a particular fetish for inventing unnecessarily complicated ways of achieving simple goals. Most other professions, so far as I can tell, are more comfortable offering simple ways to do simple things. On Wall Street, complicated ways to do simple things have bigger payoffs — for Wall Street, that is. So complexity proliferates, and it gets encrusted with jargon to impress investors into thinking there’s something special about it.

9. If stock picking is all or mostly luck, should patience (market timing) play any role in long-term investing, or should buyers take the same buying/selling approach today with the S&P 500 at 2,000 that they should have taken when the S&P 500 was trading below 700?

Being human, you naturally will be more inclined to buy more stocks at high prices than you were when they were cheap. And vice versa: When markets are depressed, you will want to sell like everybody else. In my opinion, the most reliable way for an investor to get a higher return is to be inversely emotional: to become more cautious as markets rise and to become more aggressive as they fall. One young friend of mine bought stocks with both hands during the financial crisis of 2008 and 2009, and those purchases have been like rocket fuel to her portfolio ever since.

10. What is the biggest mistake that you see investors making today?

As the analyst Raymond DeVoe said, “More money has been lost reaching for yield than at the point of a gun.” Investors everywhere want to replace the yield they have lost as falling rates have reduced the interest income generated by their portfolios, but you can’t safely get 6% yields in a 2% world. The only thing you can do that won’t raise your risk is to wait.

People hate this advice. They want to be told how they can magically get higher yields without higher risks. But there is no magic in financial markets — only people who believe there is, and who end up learning, to their pain, that they were wrong. Do you see specific examples of particularly dangerous “this time it’s different” mentality in today’s markets?

Repeat after me: It’s never different. If you’re chasing a popular speculative trend, you will get burned, maybe sooner and maybe later, but you will get burned. In the past few years, much of that mentality has chased yield — in, for example, MLP (master limited partnership) funds, business development companies, junk bond funds. And now people are chasing bitcoin and other cryptocurrencies. You can’t get higher returns without taking higher risk, period. It’s never been different, it isn’t now, and it never will be.

11. I’m a millennial who is fresh out of college and I just got my first job. I’ve never had extra cash in my life before. How should I invest it?

Put one-third in a U.S. total stock-market index fund, one-third in an international total stock-market index fund, and the final third in a total bond-market index fund. Your total annual expenses should be well under 0.2%. You can always add another couple of holdings later, but this simple portfolio will get you started. Add to it every month with an automated electronic transfer from your bank account. If one of the holdings drops in value by, say, 20%, buy more. If one ends up much larger than a third of your holdings, sell a bit (or, equivalently, add to the other two — it should save you on taxes). Otherwise, do nothing.

12. Do you believe that so many people end up disillusioned by the stock market simply because they start off with unreasonably high expectations, or do you think there’s something else at play?

I think people end up disillusioned because they don’t know who they are. They think they are investors when they are speculators. As the great financial writer “Adam Smith” (Jerry Goodman) wrote, “If you don’t know who you are, [Wall Street] is an expensive place to find out.” Anyone who ever utters a sentence beginning with the words “I need to earn higher returns because…” will be sorry; the financial markets don’t care what you need. If, instead, you take merely what the markets will give without greedily trying to get more, you will be fine in the long run. But you can’t do that unless you are patient and realistic and humble. You have to cure yourself of what I’ve called “the prediction addiction,” the belief that you can know what the markets will do next.

13. Has your view on Wall Street changed throughout the years? If so, when and why did it change?

My dad, who was a very wise man, once said, “It’s remarkable how much you need to learn in order to understand how little you ever need to know.” I spent the first 10 years or so of my career learning how investments work, and I’ve spent the succeeding 20 years learning how investors think. So many financial pundits describe investing as a kind of struggle for survival in a hostile wilderness, a battle to the death between you and the markets. That’s stupid. The battle isn’t between you and the market; it’s between you and yourself. It’s a struggle for self-control.

14. Consumers lost trillions of dollars in the 2008 crash. Can long-term investors avoid meeting the same fate in the future, or should they just accept that history will repeat itself again and they are simply along for the ride?

Well, what do we mean when we say people “lost” money? Benjamin Graham liked to use the term “quotational value,” to indicate that market prices are short-term indications, not enduring appraisals of worth. If you sold in late 2008 or early 2009, then you did lose money by locking in losses. But if you didn’t sell during the crisis, you lost quotationally, not permanently. Investing always has been and always will be risky. Stock prices fell roughly by half in 2008-09, 2000-2002, 1973-1974 and 1929-1932. They will again. I guarantee it. But I don’t know when.

Investing is an act of faith — a leap in the dark. The key is to be able to say “I don’t know, and I don’t care.” You have to know that you can’t know for sure what will happen next, and you have to be able to accept that you can’t know.

Read the rest of the column

This article was originally published on The Wall Street Journal.

Further reading

Additional resources:

Books

The Devil’s Financial Dictionary

Articles

The Devil’s Financial Dictionary: An Interview with Family Wealth Report

The Manual of Ideas: An Interview about The Devil’s Financial Dictionary

Saving Investors from Themselves

An Interview with Safal Niveshak