One of the oldest adages on Wall Street is that investors are always worried about something. This summer, the markets are writing a corollary to that old rule: When investors can’t find anything worth worrying about, they worry about why no one seems to be worrying enough.

“The global market’s ongoing low volatility should be unsettling for investors,” portfolio manager Brian Singer of William Blair & Co. wrote earlier this month, and just about every investor I’ve spoken to in the past few weeks has echoed that idea.

Tax reform is stalled, global alliances are fraying, the health-care plan is in the emergency room — yet U.S. stocks are not only at record highs but fluctuating less (by some measures) than at any time since 1993. It’s that calmness that is making many portfolio managers jittery.

I’m not so sure how much you should worry about all this.

Yes, the CBOE Volatility Index or VIX, the measure of stock-price fluctuation often called the “fear gauge,” is brushing lows set nearly a quarter-century ago. However, futures contracts expiring in 2018, a way to bet on where the VIX will head over the next year, are at prices much closer to historically normal levels. That implies traders believe today’s extraordinary calm won’t last much longer, says Joanne Hill, head of research and strategy at CBOE Vest Financial, an investment-advisory firm in McLean, Va.

The VIX dates back only about 30 years. Since 1950, according to an analysis by the BlackRock Investment Institute, stocks have fluctuated in a narrow band about 80% of the time — similar to their current behavior.

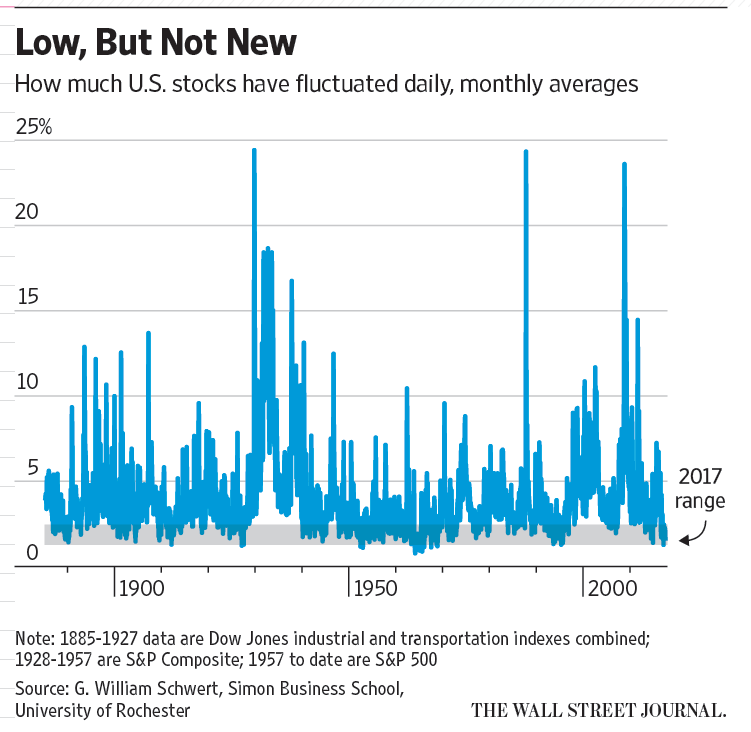

Viewed over the longer term, the recent calm is even less unusual. Counting July as if it were already over, all seven months of 2017 do rank among the least volatile on record — but they are far from the historical extremes, according to William Schwert, a finance professor at the University of Rochester.

February — statistically, the dullest point in the market’s doldrums this year — was only the 18th-least volatile among the 1,586 months since reliable data became available in 1885. So far, July is the 44th-least volatile month on record.

The early 1950s, mid-1960s and the mid-1990s, among many other periods, had volatility at least as low as today’s. Is volatility too low for the market’s own good? Does that mean that we’re in a bubble that’s bound to burst?

“I don’t think it means anything,” says Prof. Schwert, who has been studying volatility for more than 30 years. “There’s no way to determine whether volatility is too high or too low. It just is what it is.”

History shows that periods of low volatility can last surprisingly long and aren’t necessarily harbingers of bad markets to come. After multi-year periods when stocks barely fluctuated, returns have sometimes been poor, as they were after the 1929 crash, the mid-1970s and the early 2000s. But calm markets have also preceded or coincided with periods of robust returns, as in the 1950s, the late 1990s — and now, at least so far.

You might be tempted to bet against a continuation of today’s calm by buying an exchange-traded fund designed to profit if volatility jumps up. But, for complicated technical reasons, such funds can deviate wildly from the underlying performance of the VIX, sometimes delivering bloodcurdling losses. Avoid them.

What you can do is make sure the market’s calm doesn’t infect you with complacency. Stocks aren’t significantly more likely to go down after a quiet period than after a time of turbulence. But a drop will feel a lot more shocking than it otherwise would, so you had better be prepared.

Ask yourself or your financial adviser whether you have enough cash to make it through a bad market, are overexposed to stocks or have any money-losing positions you can sell to harvest a tax loss. Taking structured actions like these will help prevent you from reaching for extra risk now or suffering regret later.

Read the rest of the column

This article was originally published on The Wall Street Journal.

Further reading

Definitions of BEHAVIORAL FINANCE, DIVERSIFY, OVERCONFIDENCE, RISK, and VOLATILITY in The Devil’s Financial Dictionary

Chapter Eight, “The Investor and Market Fluctuations,” in The Intelligent Investor

Chapter Seven, “Fear,” in Your Money and Your Brain

G. William Schwert, “Why Does Stock Volatility Change Over Time?“

Robert J. Shiller, “The Volatility of Stock Market Prices“

Robert J. Shiller, “Speculative Asset Prices” (Nobel lecture)

Dave Nadig, “Understanding VIX ETFs: Careful What You Wish For” (ETF.com)