Just about everybody claims to be a long-term investor, even though most professional and individual investors seem to have about as much patience as a bunch of teenagers competing in a Red Bull chugging contest. Why are people so impatient when they all insist that patience is a virtue and that they themselves are virtuous? These questions have plagued me for a long time. I’m still patiently searching, and hoping, for some answers. If I keep at it long enough, maybe I’ll figure it out. Here, from my archives, is a piece I wrote about the difficulties of patience. Can it have been less than 14 years since I wrote it?

The Rip van Winkle Portfolio

Is it possible to invest so reliably that you won’t have to change anything for the next 20 years? It’s at least worth a try.

Money Magazine, March 2004

Invest for the long term. That’s what everybody always says we all should do. But if it’s such a great idea, how come nobody seems to do it? According to Morningstar, the average U.S. mutual fund sells its typical stock only 11 months after buying it. Annual turnover on the New York Stock Exchange also exceeds 100%, meaning every share of the typical stock changes hands more than once a year.

The horrible market losses of the past few years seem to have made many people question the value of a long-term outlook. In a recent survey of investors for Charles Schwab, 42% of the 515 participants said that “investing for long-term returns rather than short-term gain” is not much more important to them now than it was three years ago.

Has this epidemic of attention deficit disorder made anyone richer? The evidence is disturbing:

- Studies by Morningstar and other researchers have shown that among most categories of mutual funds, those that trade the fastest earn less than those that trade least often. Like someone stuck in quicksand, the typical fund manager sinks in deeper the faster he struggles to get out.

- On average, the percentage of mutual funds that beat the market is lower than it was back in the Jurassic days when funds held stocks for years at a time.

- The money managers fired by big institutions like pension funds and university endowments usually go on to outperform the firms that replace them. No wonder the institutional process of selecting money managers has the cynical nickname of “hire high, fire low.”

So here we all are — from the boards of trustees who run multibillion-dollar endowments to the people who manage mutual funds and the people who own them — acting as if the only way to invest for the long run is by constantly juggling our portfolios. Most of us know better, yet we just can’t help ourselves. Add up the effects of investing ADD, and it’s clear that the financial markets desperately need a massive dose of Ritalin.

As if the Long Term Mattered

For years, I’ve been in search of what I consider the holy grail of investing: not a good way to get rich quick, but a guaranteed way to get rich slowly. I’ve taken to calling this elusive goal the Rip Van Winkle portfolio. You may remember from the short story by Washington Irving that Rip went to sleep for 20 years and awoke to a world that was, all at once, shockingly changed and hauntingly familiar.

What if each of us had to invest so that, if we left our portfolios untouched for two decades, we could be assured in the end of having all the money we would need? I think it’s a useful exercise; investment horizons, like muscles, can only benefit from regular stretching.

So I was delighted last fall when I wangled an invitation to an investing conference with this theme: “As if the Long Term Really Did Matter.” It turns out that the leading pension fund for educators in the U.K. (which goes by the very British name of the Universities Superannuation Scheme, or USS) had come up with a very British idea: Let’s make a game of it. The USS created a scenario in which institutional investors controlling $35 billion wanted the money managed in a “genuinely long term” and “genuinely responsible” way.

The notion was to challenge investment managers and thinkers to come up with innovative ideas on how money ought to be managed when the investing horizon is decades instead of days. The winning entry would earn…a cut-glass trophy. (The $35 billion was imaginary.)

Raj Thamotheram, the USS executive who cooked up the competition, explains the idea this way: “The system is broken. Everyone blames someone else for why money is not invested for the long term. Everyone has a ‘Yes, but.’ We wanted to start off with a clear blue sky and see how we might start repairing the system so it could achieve the goals we’re all here for.”

The USS announced the contest last spring. In the end, 88 entries came in from money managers, professors, consultants and individuals. Nine came from Australia; a grand total of six came from the U.S. Thamotheram recalls, “The typical reaction we got from the U.S. was, ‘What the hell does it matter? The long term is only a series of quarters.’ “

What a sad commentary on how antsy American investors have become!

At the USS conference in Amsterdam last fall, the American investment industry was even more conspicuous for its absence. The 102 attendees hailed from at least 10 countries — but only three came from the U.S., and one of them was me. That’s a shame; the conference aired some fascinating ideas that can help investors stretch their horizons.

The Only Goal

One entry after another made this key point: The purpose of a pension plan is not to outperform the market or its competitors. Its only goal is to cover its liabilities — by ensuring that retirees get the benefits they will need to live on. Likewise, you do not succeed as an investor by beating the market or getting a higher return than Wally Finkbeiner’s brother-in-law. You succeed by staying on track to amass more money than you will need to cover that housing down payment, college tuition, retirement or whatever ultimate liabilities you are saving and investing for.

Constantly measuring the short-term returns of your assets distracts you from the only real goal: funding your long-term liabilities. So you should cut back those nervous checkups on your investments — the less often you look, the less volatile they will seem.

That, in turn, should help keep you from dumping your investments at the first whiff of trouble–the worst mistake most professional investors make. As the great investment thinker Benjamin Graham put it, “The investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into a basic disadvantage.” The farther you can stretch your horizons, the better you will fare in the long run — and the less stress you will suffer in the short run.

Rewarding the Right Thing

The first principle of fees for service is that you get what you pay for. When you hire a money manager, what you want to reward is long-term performance. Instead, management fees at most mutual funds are designed to reward short-term growth in a fund’s size — which rarely does you any good.

The winning entry in the USS competition — from London-based Henderson Global Investors — pointed toward a solution. For a fund’s first five years, fees would be minimal. After that, the managers would be paid primarily for performance, earning a bonus if they exceeded a target rate of return over the preceding five years. Another good idea from the competition: The bonus would be calculated each month, not just on Dec. 31, when many funds have a mysterious habit of beating the market for the day. Now that’s fair.

In the U.S., unfortunately, such fees are as rare as they are fair. Among major firms, only Fidelity and Vanguard regularly charge more when their funds outperform and less when they under perform. If U.S. firms truly believe in the virtues of long-term investing, they should adopt performance fees.

Another thing becomes clear when you stretch your mind toward the year 2024: It seems silly to put much effort into studying which mutual funds have the best managers. Two decades from now, how many of them are likely to be around? Some of today’s “star managers” will be hired away by other mutual funds; some will quit to run a hedge fund; some will retire; some will even die of old age. Very few will still be running the same fund in 2024.

Spare yourself the trouble of chasing managers and returns from one fund to another. By holding an index fund, you automatically own all the stocks or bonds in a market benchmark, all the time — no worries about whether the manager is fickle, fading or mortal.

What Would Rip Do?

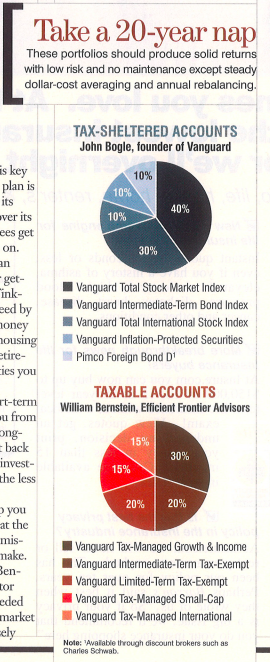

A lot of other things can change in 20 years. As John Bogle, founder of the Vanguard funds, puts it, “What could be more absurd than the idea that the long term is more predictable than the short term? We can’t be quite as secure about America’s position in the world 20 years from now as we can be today.” Therefore, Bogle thinks, it’s prudent to hedge against the possibility that other countries might grow faster than the U.S. over the next 20 years. That’s why Bogle’s Rip Van Winkle portfolio includes international stocks and bonds — assets that he has traditionally shunned.

Picks for Patience

If you’re investing for the next 20 years, you can hold assets that might earn a premium return for patient investors. That could steer you toward emerging markets or value stocks (preferably in a retirement account, where they won’t generate excessive tax bills). Small stocks might also pay off over the very long run, as money manager William Bernstein of Efficient Frontier Advisors suggests in his Rip Van Winkle portfolio.

If you like picking your own stocks, try mentally marking a portion of your money — say, 10% tops — with the words DO NOT DISTURB. Put the stocks you think have the most promise in that long-term account. If you’re right, and at least one of them does turn out to be the next Microsoft, then you’ll make a lot more money by leaving them alone for 20 years than by trading them or selling too soon. If you’re wrong, and they turn out to be a bust, the rest of your money should remain unscathed.

Finally, as USS pension fund’s Thamotheram argues, companies helping solve the world’s biggest problems may turn out to be the most profitable in the long run. Whatever your politics, there may be a “socially responsible” fund that can put your money to work making the world a better place in your eyes. Just watch your wallet; if a fund charges more than 1% in annual expenses, it isn’t worth the privilege.

Read the rest of the column

This article was originally published on The Wall Street Journal.

Further reading

Amit Goyal and Sunil Wahal, The Selection and Termination of Investment Management Firms by Plan Sponsors

Brad M. Barber and Terrance Odean, Trading Is Hazardous to Your Wealth: The Common Stock Investment Performance of Individual Investors

Josef Lakonishok, Andrei Shleifer and Robert W. Vishny, The Structure and Performance of the Money Management Industry

Richard H. Thaler et al., The Effect of Myopia and Loss Aversion on Risk Taking: An Experimental Test

Additional resources

Books

The Devil’s Financial Dictionary

Benjamin Graham, The Intelligent Investor

Articles

Amit Goyal and Sunil Wahal, The Selection and Termination of Investment Management Firms by Plan Sponsors

Brad M. Barber and Terrance Odean, Trading Is Hazardous to Your Wealth: The Common Stock Investment Performance of Individual Investors

Josef Lakonishok, Andrei Shleifer and Robert W. Vishny, The Structure and Performance of the Money Management Industry

Richard H. Thaler et al., The Effect of Myopia and Loss Aversion on Risk Taking: An Experimental Test

Articles by Jason Zweig

So You Think You’re a Risk Taker?

When the Stock Market Plunges, Will You Be Brave or Will You Cave?

Here Comes the Slow Stock Movement

The Market Really Is Different This Time

Use the News and Tune Out the Noise

Bogle: Still Scolding After All These Years