Image Credit: “Women holding parts of the first four Army computers,” 1962, Wikimedia Commons

{kind=link}

Readers always surprise me.

I thought my column two weeks ago, on the Crash of 1929, would provoke a flood of tweets and comments and emails saying “That could never happen again!”

Almost nobody said that.

Instead, many readers claimed that it wouldn’t have taken the typical investor very long to break even on stocks after the Great Crash. I had written: “The Dow didn’t surpass its 1929 high until Nov. 23, 1954, a quarter-century later. That doesn’t include reinvested dividends, but most investors surely took their dividends as cash in those days.”

My latest column looks again at that argument, but a lot of the research I gathered for it wouldn’t fit at WSJ.com or in print. So here are additional materials I didn’t have room for.

When I say “Total return is a technology,” what do I mean?

First, to match the total return of a market, you have to be diversified.

Next, you have to be able to reinvest your dividends or other investment income back into the market efficiently.

And your costs to diversify and to reinvest dividends have to be low enough that the pursuit remains worthwhile.

Unfortunately, none of those conditions held until recent decades. Diversification used to be incredibly expensive and vanishingly rare. Reinvesting dividends was also cumbersome and costly. Commissions, on stocks and mutual funds alike, were extraordinarily high.

Researchers at Vanguard Group recently estimated that from the 1980s onward, the shift out of individual stocks and into mutual funds provided about $730 billion cumulatively in diversification benefits to U.S. investors.

Could you even have owned the S&P 500 after the Crash of 1929? Of course not. Jack Bogle didn’t invent the index mutual fund until 1976.

Not even institutional investors could buy an S&P index fund until 1971! (See my colleague Bob Hagerty’s obituary for Bill Fouse here.)

Could you have owned a diversified stock fund that would have more-or-less replicated the return of the S&P 500?

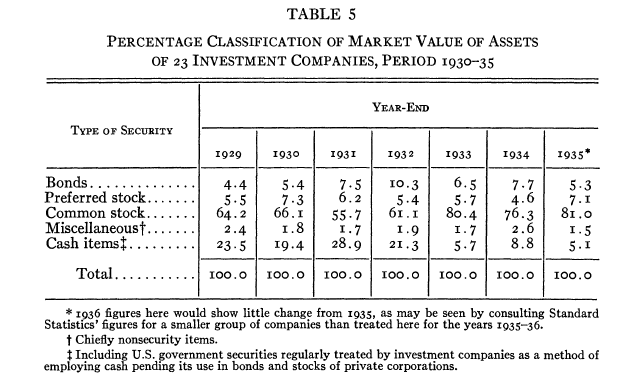

Yes, with heavy emphasis on the “less.” According to a study published in the Journal of Business in July 1938, most funds owned a mix of stocks and bonds:

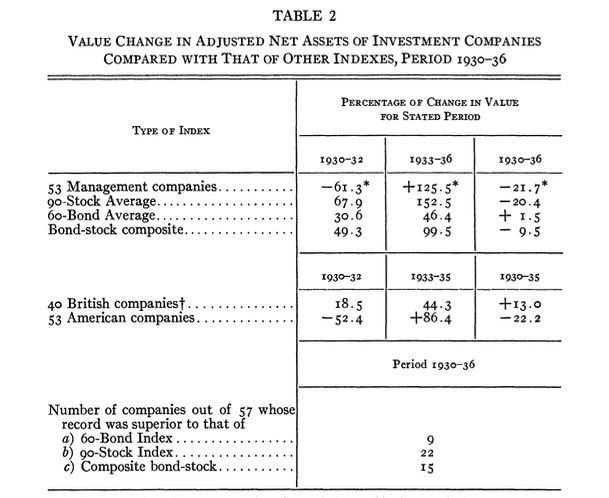

Note that the funds raised cash as the market bottomed, and drained it as the market went up. Instead of buying stocks when they were cheapest, the funds did the opposite: They bailed out at the bottom, so when stocks rebounded the funds couldn’t participate fully in the gains. No wonder they came nowhere near matching the S&P 500’s performance:

Those numbers don’t include “loads” or sales charges, which in the 1930s averaged 5.5% on investment trusts (the equivalent of today’s closed-end funds) and ran as high as 9% to 10% on mutual funds.

In fact, you had slightly less than a 50% chance of staying invested at all if you’d bought a fund around the Crash of 1929. Of the 1,272 investment trusts (the equivalent of today’s closed-end funds) launched between 1927 and 1936, only 559 survived as of Dec. 31, 1936, according to a report by the Securities and Exchange Commission in 1940.

Longer-term returns weren’t a lot better. A study in the April 1952 Journal of Business by George Moffitt found these results from the end of 1929 through early 1951, a period over which the predecessor index to the S&P 500 was precisely flat (not counting dividends):

“Well, look at that,” you might say. “Seven out of 10 funds beat the market!”

True enough, but about 150 mutual funds existed at that time, and Moffitt cherry-picked the ones he knew, with 20/20 hindsight, had the best performance. The only sensible way to interpret his finding would be: “Seven out of about 150 funds beat the market” (or under 5%). And two of the best, the Loomis Sayles and Scudder funds, were extremely small, with only a few investors.

Furthermore, while Moffitt factored sales charges into his calculations of capital appreciation, his income figures don’t include loads.

Incredible as it might sound to investors today, you used to have to pay commissions to reinvest dividends.

Back when I became the mutual-funds editor at Forbes magazine in 1992, a few fund companies were still charging to reinvest dividends (typically 4% and up). That was barely over 25 years ago.

From the 1920s through the 1970s, that wasn’t unusual; it was the norm. Most mutual-fund companies charged their investors sales loads to reinvest dividends.

Think about that for a moment. Fund investors could take the dividends as cash at no charge (other than having to wait a week or more for the check to arrive), or they could pay a sales load to reinvest the dividends.

Who in their right mind would pay up to 10% to reinvest a dividend they could cash for free?

It’s possible that some mutual-fund investors reinvested their dividends anyway (or the roughly 90% of their dividends left after the sales load). It’s also possible that some of them jumped across the Grand Canyon carrying a brick in each hand. Anything is possible. But those two scenarios seem about equally probable.

Of course, many investors did buy stocks directly, even through the depths of the Great Depression. How likely was it that they reinvested those dividends?

The average household earned about 6% of its income from dividends in the late 1920s, according to economist Willford Isbell King (see p. 196 at this link). Although that number is surely skewed by wealthier households, it’s hard to imagine many families during the Great Depression being willing to take the cash their dividends generated and reinvest it into more shares, rather than spend it to fund their urgent, immediate needs.

That was especially true because the total dividends paid by American corporations plummeted during the Great Depression. Many readers protested to me that dividend yields went up, but that’s only because share prices fell even farther. According to a 1956 study by the National Bureau of Economic Research, total dividends paid to individual shareholders reached a high of $520.4 million in dividend payments in September 1929. By April, 1934, that number fell to $149.7 million, a 71% decline. Total dividends paid to individuals didn’t regain their 1929 level until August 1946.

Numbers from the Internal Revenue Service tell a similar story of dividends drying up: Individual taxpayers reported $4.79 billion in “dividends on stock of domestic corporations” for 1929 and $1.56 billion for 1933, a 67% decline.

You can see the epic collapse of dividend payments in this graph, from the Federal Reserve Bank of St. Louis:

As late as 1952, economist Lewis Kimmel found that “a substantial portion” of widows over the age of 60 said that dividend income from the stocks their husbands had bequeathed to them “constitutes their main source of support.” Such shareholders wouldn’t have been reinvesting dividends; they needed the cash income to live on.

Those numbers don’t account for changes in purchasing power. Deflation was severe in the 1930s, so cash became more valuable over time — not less, as it does during periods of inflation. Across time, worldwide, people have hoarded cash during deflationary periods for just that reason. So it’s farfetched to think that most investors would rather have reinvested dividends than take the cash upfront.

To be sure, some companies — especially electric utilities, telephone companies and some industrials — did run dividend reinvestment programs through which individual investors could use their quarterly dividends to buy more shares at low or no cost (and, sometimes, even at a discount to market price). To the best of my knowledge, there’s no data on how much money investors plowed back into more shares using these programs from the 1920s onward. The likeliest guess, though, is not very much. And they don’t seem to have taken off until the 1960s and 1970s.

What about individual investors who simply bought and held individual stocks? Trading costs were extraordinarily high — up to 6% — on small investments of less than 100 shares per stock, as mutual-fund broker Murray Simpson testified to the U.S. Senate in 1967:

That didn’t even count the bid-ask spread, or the scalping a broker would give you by selling to you at a disadvantageous price. That probably would have cost you close to another 1%, according to Columbia finance professor Charles Jones.

I know first-hand how painful these costs were in the bad old days. I bought my first stock in 1976 and paid roughly 5% in commissions. I presume I also paid a spread of another 1% or so.

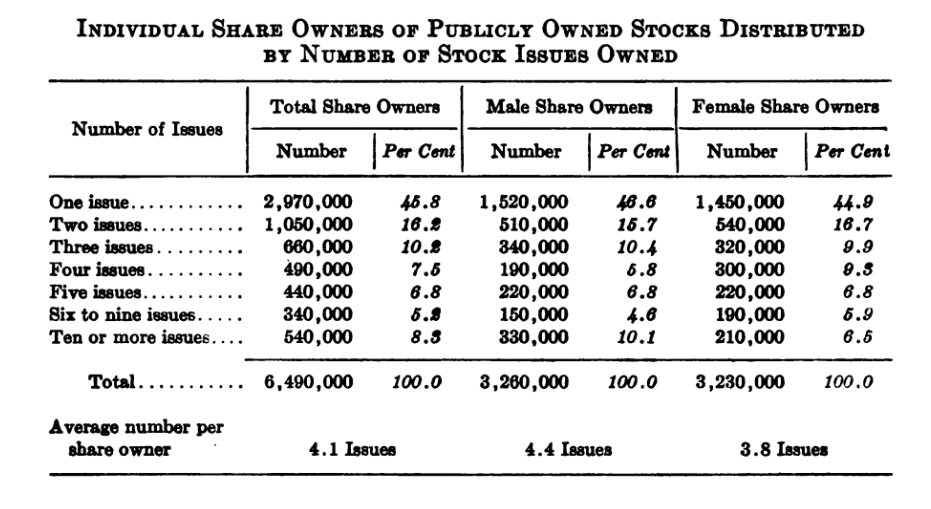

Most individual investors who bought stocks didn’t diversify widely, probably because it was so costly. Lewis Kimmel found in a survey conducted in March 1952 that almost half of all investors owned only a single stock and that the average investor owned four:

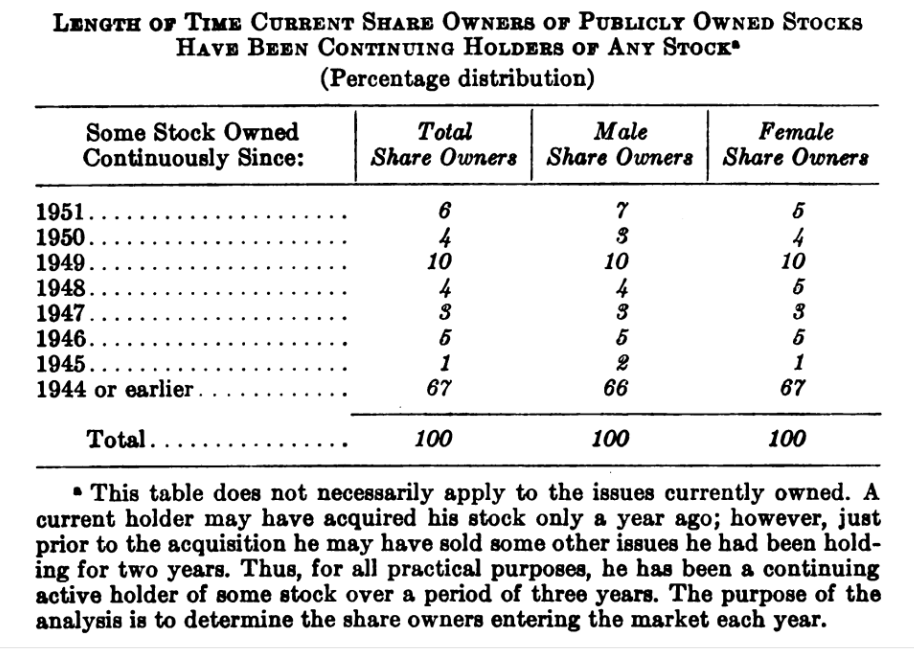

Kimmel did find that about two-thirds of investors had held at least some shares since at least 1944:

Unfortunately, Kimmel didn’t ask how many had been holding at least some shares continuously since 1929. I’m not aware of any source that would enable us to determine how many people stuck to a buy-and-hold strategy even after the bear market destroyed almost 90% of their wealth. In what behavioral economists call the “disposition effect,” investors who have lost a lot of money are often reluctant to lock in their losses by selling. After the Crash of 1929, many investors even seemed to be planning to take their stocks with them when they died. As The Wall Street Journal‘s “Broad Street Gossip” column said on Nov. 1, 1930:

So add it all up — or should I say “subtract it all out”? — and it’s extraordinarily unlikely that the typical investor earned the total return of the stock market in the decades before the 1970s.

Total return isn’t just an investing concept; it’s also a technology. The advent of the index fund in the 1970s made diversification systematic and cheap; the development of electronic trading slashed brokerage costs to the bone. Only in recent decades has the technology of total return been sufficiently developed for the typical investor to reinvest dividends conveniently and at low cost.

Jack Bogle is remembered as the father of the index mutual fund, but it’s only a slight exaggeration to call him the father of total return. By making index funds available to virtually anyone with spare cash and enabling every investor to plow dividends back at zero cost, he made it possible for anyone to match the market’s return in practice, not just in theory.

Buy-and-hold investing can take longer to pay off than many investors realize, but at least they can be assured of capturing virtually all the return that the market does produce.

That’s huge historical progress over the way our ancestors had to invest, and no one today should take it for granted.

Further reading

Benjamin Graham, The Intelligent Investor

Jason Zweig, The Devil’s Financial Dictionary

Jason Zweig, Your Money and Your Brain

Jason Zweig, The Little Book of Safe Money