In July 2009, journalist Matt Taibbi invoked an indelible image when he described Goldman Sachs as “a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money.”

The metaphor has a longer history than you might realize.

Squids and octopi inspired widespread terror in the 19th century, when marine biology was a crude science and ignorance abounded. In Moby-Dick, Herman Melville describes a giant squid as

the most wondrous phenomenon which the secret seas have hitherto revealed to mankind. A vast pulpy mass, furlongs in length and breadth, of a glancing cream-colour, lay floating on the water, innumerable long arms radiating from its centre, and curling and twisting like a nest of anacondas, as if blindly to clutch at any hapless object within reach. No perceptible face or front did it have; no conceivable token of either sensation or instinct; but undulated there on the billows, an unearthly, formless, chance-like apparition of life.

Tennyson’s sonnet “The Kraken” describes ominous squid-like creatures that “winnow with giant arms the slumbering green.” And Victor Hugo, in his novel Toilers of the Sea, described the octopus as “glue filled with hatred”:

if terror be an object, the octopus is a masterpiece…. It is the pneumatic machine attacking you. You have to deal with a vacuum furnished with paws. Neither scratches nor bites; an indescribable scarification. A bite is formidable, but less so than a suction. A claw is nothing beside the cupping-glass. The claw means the beast entering into your flesh; the cupping-glass means yourself entering into the beast….The tiger can only devour you; the octopus, oh horror! breathes you in. It draws you to it, and into it; and bound, ensnared, powerless, you feel yourself slowly emptied into that frightful pond, which is the monster itself. Beyond the terrible, being devoured alive, is the inexpressible, being drunk alive….

Many people in the late 19th century accepted the farfetched notion that giant squid — which live roughly half a mile down deep in the oceans and surface so rarely that no living specimen was ever photographed until the early 2000s — preyed on human flesh.

And the octopus, with its ramification of menacing tentacles, became a common symbol of monopoly in cartoons of the day, as you can see here and here.

Frank Norris’s novel The Octopus (1902) belabored the metaphor of a powerful railroad wrapping its tentacles around the lives of people struggling to make a living.

It was against this backdrop that a leading broker compared Wall Street to cephalopods.

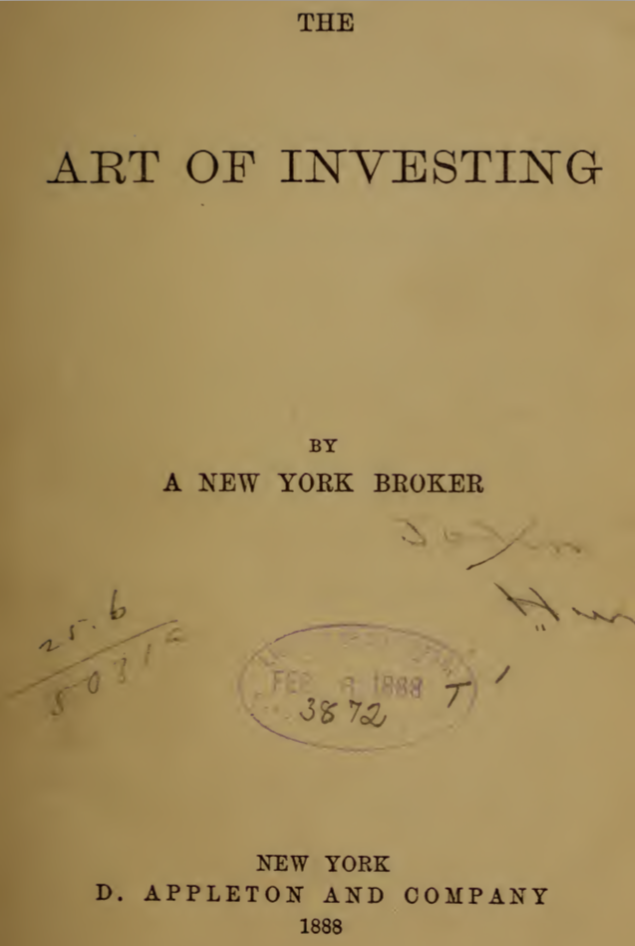

The Art of Investing, published in 1888 as the work of “A New York Broker,” was written by John Ferguson Hume (1830-1909). Born in upstate New York, Hume graduated from Ohio Wesleyan University at age 20, became an Ohio state legislator, and then moved to St. Louis, where from 1860 through 1865 he was editor of the newspaper that became the St. Louis Globe Democrat. Hume became a prominent abolitionist in a state viciously divided over slavery and served as a Missouri delegate to the 1864 Republican national convention. In the 1870s he moved back to New York and, by 1885, was running a brokerage firm.

The first 100-plus pages of Hume’s book are a dry enumeration of the stock and bond markets of the day. But in his second chapter, Hume lets it rip. As a former newspaper editor and leading abolitionist, he knew how to fulminate from a bully pulpit, and here he goes off on a fire-and-brimstone tirade against the crooked practices and shoddy securities of the day.

We should bear in mind that a tradition of such criticism dates back at least to Thomas Mortimer’s Every Man His Own Broker (London, 1761): Typically, the banker or broker writing such an investing handbook warned readers in vivid language about the hazards of devious markets on the one hand and, on the other, held himself out as an oasis of honesty. Hume, like other broker-authors before him, may have been passionately sincere in his criticisms and, at the same time, intentionally using his candor as a marketing gimmick for his brokerage. (The “Appendix” to Hume’s book is essentially a self-advertisement.)

I have left the original text unchanged, other than to introduce more paragraph breaks for easier online reading and to put some of what I regard as Hume’s best observations in bold type.

The references to devil-fish, octopi, and squid are only part of the pleasures here. Hume mocks the idea of market efficiency, ridicules Wall Street’s tendency to trade on rumors and blow them out of all proportion, highlights the pathetic habits of traders moving in herds like livestock, describes the perennial chase after past performance, warns that volatility can be as bad for investors as it is good for brokers, and emphasizes the distinctions between long-term investment and short-term speculation. But I’m sure you will be struck, as I was, at how vividly he develops the metaphors of Wall Street as “devil-fish” and “cuttle-fish,” reaching its tentacles across the land to crush businesses and squirting black ink to blind and confuse speculators.

Above all, Hume could write.

And you should read. Enjoy!

CHAPTER II.

SPECULATING *

* The following chapter appeared in “The Forum” for October, 1886, under the title of “The Heart of Speculation.”

NEW YORK has no more entertaining public exhibition than its Stock Exchange. It is one of the show-places of the city. The visitor who, for the first time, looks down from a gallery upon its members in the act of transacting business, is astonished at the apparent confusion he witnesses. He seems to have entered a mad-house. The idea that the market values of our leading securities should be determined by what appears to him to be a howling mob of incurable lunatics, is incomprehensible. But if nothing could be said against the Exchange, which is simply a big bazaar for the sale of bonds and stocks, except its tumultuousness and the seeming lack of dignity among its operators, criticism would have in it but an indifferent target for its shafts. Much graver questions grow out of its existence. Is it a harmless institution? Is it a public blessing? Is it a public curse?

As a great central mart for current securities, it would be unobjectionable. There is no reason why bonds and shares should not be publicly dealt in, and in large quantities, as well as dry-goods; as well as corn and cotton and beef and kitchen vegetables. If the Stock Exchange was intended for or restricted to the bona-fide buying and selling of bonds and shares, not a word could be justly said against it.

But is that its business? Unfortunately, no. Its chief occupation is wagering on stocks: its members, while going through the forms of buying and selling, simply bet their money, or somebody else’s money, upon the rise or fall of the shares they select, as they would upon the shiftings of cards or dice. The Exchange, while having a share of legitimate business, is chiefly an immense gambling establishment.

Its members are divided into two classes — those who execute commissions for others, and those who deal on their own account. It is needless to say that among the latter are the boldest and sharpest speculators of the day. The careers of these men can be sketched in very few words. Through the exercise of superior native wits or the accident of extraordinary luck, they flourish marvelously for a time; but only, as a rule, to lose their heads and their balance at last, and go down — often through a single disastrous transaction — faster than they went up. There are exceptions. Some flourish to the end, dying — generally young — or retiring with estates unbroken. But they are exceptions.

Wall Street is a place where a few fortunes are made and a great many are lost. The stories of its magnificent triumphs, and of its equally magnificent wrecks, read like tales from the “Arabian Nights”; some of them like passages from Dante’s “Inferno.” Wall Street has had its suicides by the dozen, and it will have plenty more. It would not be Wall Street without surprises.

And yet there is a singular sameness in the ordinary broker’s experience. He runs an exciting, if at times a rough and stormy, career, snatches or seems to snatch a good many pleasures by the way, makes and breaks with about equal abandon, wrecks his health in a hurry, dies early and suddenly, and then — well, then, when his affairs come to be settled, there are found to be large blocks of utterly worthless shares, perhaps a fast horse or two, a two-wheeled vehicle and trappings to match, some costly souvenirs, and very few solid assets, and the business is closed in bankruptcy. Poor fellow, everybody has forgotten all about him!

Of the ordinary Wall Street speculator, however clever or however favored for a time, it is perfectly safe to say that, if he lives long enough and sticks to the business, he will finally come to grief. But how about Vanderbilt père, who was more or less of a “Wall Street operator” all his many days, and a few other not wholly dissimilar if less conspicuous examples?

Ah! that brings us to a view of some of the interior workings of the New York Stock Exchange that the public has little conception of, and which alone will give a correct understanding of its real character. The popular idea is that the Exchange has upon its list, to be dealt in, all, or nearly all, prominent stocks and bonds of acknowledged value, impartially selected and solely because of their merits.

There could be no greater misconception. We look there in vain for the shares of the Pennsylvania Central, whose stock has not a drop of water in it; of the Baltimore and Ohio, whose paper, notwithstanding some mistakes of its managers, is equally solvent; of the Boston and Providence, the Boston and Albany, the New Haven and Hartford, the Maine Central, and of dozens of other corporations whose management is unexceptionable, and whose securities are among the choicest investments.

But if there is a company with a speculating board of directors, and whose stock has been watered until it will float a respectable navy, its shares are pretty sure to be found on the Exchange’s list. Or if there is a company that is absolutely controlled and directed by some particularly active and conspicuous manipulator, its stock may be looked for at the same place. There has never, apparently, been any difficulty in a big stock operator getting his issues upon the list. What has been the result? Simply that the most abominable rubbish has been unloaded upon the public.

Much, but not too much, has been said in condemnation of stock-watering; of the production of corporate certificates representing little or no cash investment, and which innocent persons are led to purchase in the belief that they are getting full values. But how is it that these fraudulent issues can be marketed, and the producers escape legal responsibility for the impositions practiced?

Here is where the Exchange’s work comes in. The Exchange is the conduit through which the water is safely carried into the investors’ pockets. When it takes the stock upon its list, the Exchange becomes practically the seller, supplying the machinery and the means of transfer, and it guarantees nothing. Whoever buys at its board is understood to take all risks, no matter how much deception is used. He may be utterly victimized — often is so — but he has no redress. Here is the medium through which the over-issues have been marketed. But for the Exchange’s instrumentality, the facilities it has furnished, those stupendous stock-watering frauds which have become historical never could have been successfully consummated.

Once on the Exchange’s list, there has never yet been a stock so worthless that, with a shrewd manipulator behind it, it could not be unloaded. The process has been a simple one: First, there are “washed” — singular how the idea of water runs through all stock operations — or prearranged sales of the stock. Outsiders are then told that there is money in it, and they begin to buy. The stock is duly “supported” — an indispensable precaution — that is, it is taken at quotation prices when offered by outside owners, and so up and up it is marked, the speculative public taking large blocks in the belief that it is going higher, and with little thought of its actual value, until there comes a time when, the original supply being exhausted, the shares are no longer supported, and down, down they go.

The real value of the stock has little to do with its negotiation. In the light of that explanation, there is no difficulty in comprehending how certain great railroad magnates, who are leading operators in Wall street, have amassed such colossal fortunes. They have been stock manufacturers as well as stock-dealers. The New York Exchange has been their field of operations — their market-place. Through it they have sold their wares. Had they, like ordinary speculators, confined themselves to other people’s goods, it is questionable whetherthey would have grown exceptionably rich. They might have become poor, as the most of their associates have done. But when, with consciences conformable to their opportunities, they had the means of selling water at high figures and in practically unlimited quantities, it is no wonder that their fortunes swelled to fabulous proportions.

A glance at the Exchange’s list tells the whole disgraceful story. What a column of tatterdemalions it parades! It looks as if, in making up its assortment, the listing committee had gone into the highways and by-ways, with orders to bring in the lame, the halt, and the blind.

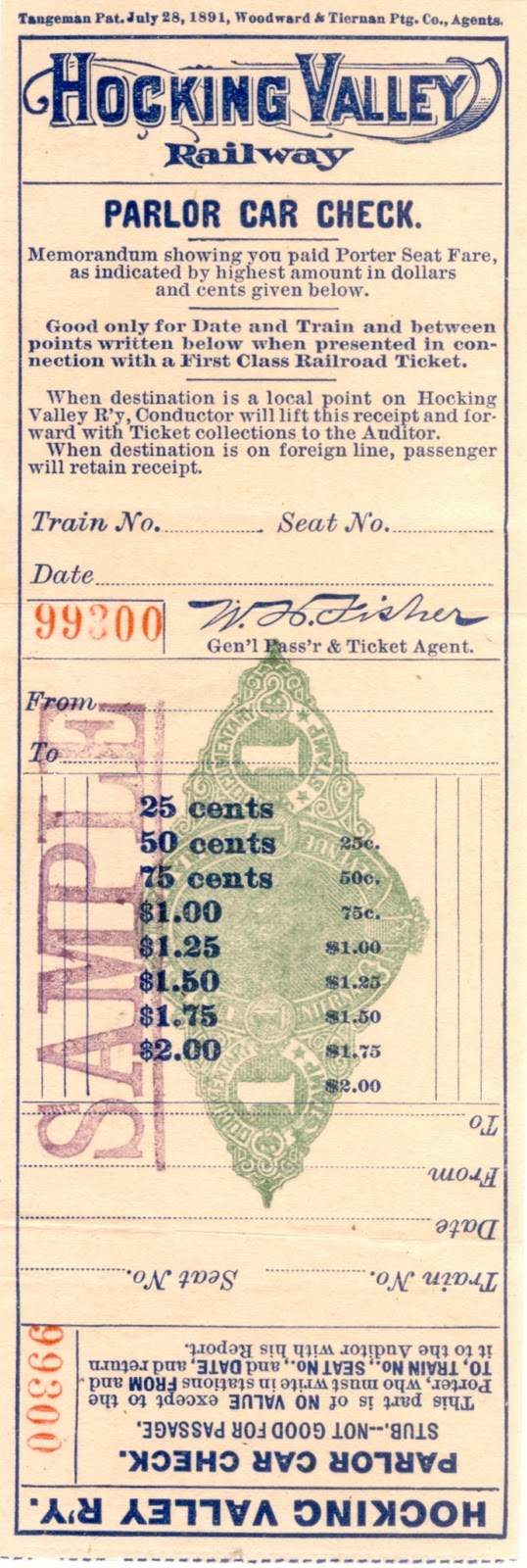

Wabash is there, Denver and Rio Grande is there, Hocking Valley is there, Texas and Pacific is there, Bloomington and Western is there, Nickel Plate is there, West Shore is there, the whole noble army of frauds that once flourished so magnificently and bled the public so profusely, is there.

Consolidated Gas, with thirty-five millions of stock that, from official investigation, would appear to have been evolved from a cash investment of less than twelve millions, is there, of course. It is a new accession, and shows how naturally inflated and adulterated securities seek the Exchange’s forum, and how readily they are admitted.

The Exchange has a committee to pass upon applications for listing, and which, in theory, excludes unworthy issues. It is supposed to act as a sieve; but certain it is that, sieve-like, it is no obstruction to the passage of water. While its bond-list, as a whole, is much more respectable than its stock-list, it is noteworthy that the Exchange’s dealings are principally in the speculative issues — the second and third mortgages, the incomes, the land-grants, and other junior or discredited securities. These are the driftwood of the market, which nobody buys to keep, because, yielding little or no income, they are of no account as investments; and they are bid up or bid down, according to the course of speculation at the time. When actual investors wish to buy, as a rule they go to bankers and dealers who have nothing to do with the Exchange and pay very little attention to its quotations.

Oh, how gayly the business of making and marketing securities was but recently going forward in Wall Street! The inflation period that followed the depression from 1873 to 1879 was the golden era of stock speculation. The Exchange fairly rioted in profitable traffic.

The public was supposed to be crying for shares, and the magnates of that institution were doing their best to meet the demand. They succeeded pretty well. Some of them built new roads and stocked and bonded them for only four or five times their actual cost. They sought strange fields for their ventures — in the wilderness, upon the desert plains, among the mountain-peaks. They overleaped the national boundaries and rushed pell-mell into Mexico; and when all available openings were filled, they entered upon the work of “paralleling ” — constructing new roads by the sides of old ones.

The purpose of it all was the production of paper to be dealt in “at the board.” It was bonds, bonds, bonds; stock, stock, stock; water, water, water. Millions upon millions of so-called securities were manufactured, costing little more than the blank paper upon which they were stamped and the mechanical labor bestowed upon it, and dumped into the hopper of the Exchange, to be by it stirred up and turned over a few times, and then systematically worked off on the great investing public.

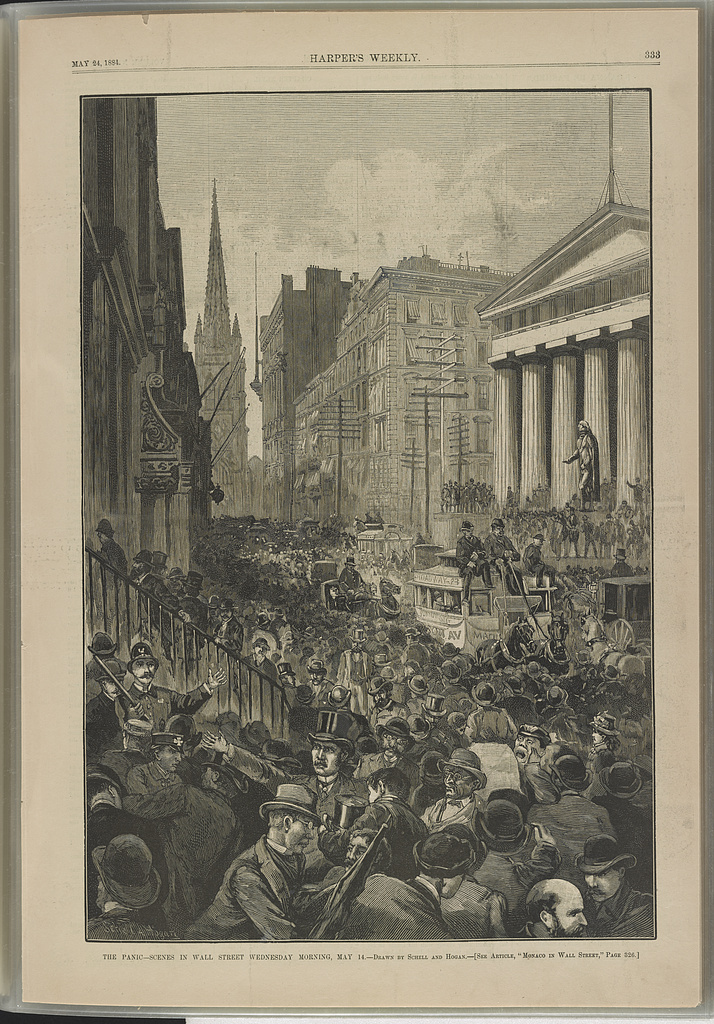

Very well does the writer, as well as a good many others, remember what it all came to; how on a bright day of May, of the year 1884, pandemonium, in the form of a panic, entered Wall Street; how the great throngs that gathered there and filled all available spaces surged and seethed like troubled waters; how great bankers and leading business men ran wild-eyed and bareheaded through the streets; how mobs of half-demented people crowded round brokerage-houses, richly-dressed women and gray-haired men among them, weeping and wringing their hands; how surrounding the doors of suspected banks were groups of idlers who, with the true instinct of Wall Street denizens, were betting their money on the length of time their doors would remain open; how about the remorseless “tickers” in brokers’ shops were gathered crowds of excited men, tremblingly watching the course of stocks that seemed to be going down, down to perdition, the water they contained suddenly turning to hydraulic pressure to crush them. Those who saw that spectacle in all its grim and terrible seriousness will witness nothing to match it this side of the “Inferno.” Ah! the New York Stock Exchange then gave its patrons a treat many of them will not soon forget.

But the Exchange, with all its shortcomings, is at least useful if not necessary in supplying quotable values and giving stability and tone to the business of the country. Is it? Let us see.

On the 1st of March, 1884, Delaware, Lackawanna and Western stock sold on the board at 133 1/8. In January following it brought at the same place only 82 5/8. The next December it was up to 129 5/8. “Lackawanna” is an old, conservative company, lightly capitalized, with an established business; a regular, uniform dividend-payer. Intrinsically the value of its shares has not varied in the past five years. “St. Paul” is another stock that, apart from speculation, should not change. Yet in 1883 it sold “on ‘Change” as high as 108 1/2, in 1884 down to 58 1/4, and in 1885 was back to within one per cent of par. In one half hour during the May panic of 1884 the securities on the Exchange’s list shrank in quotations over $100,000,000; in one day nearly $300,000,000.

Not much stability, not much reliability there! Either prices had been much too high or they went much too low. The Exchange in the one case or the other, if not in both, failed to hold them at the proper level.

Nor in this is there anything remarkable. Wide and sudden fluctuations are necessary results of the Exchange’s methods. Its members are supposed to be divided between “bulls” and “bears” — those who try to advance prices and those who try to depress them; but all are as likely as not at one time to be bulls and at another bears.

They have their stampedes. No drove of cattle upon the Western prairie is more subject to sudden scares and erratic rushes than they are. Indeed, a wild herd of steers, with horns uplifted and tails in the air, charging across the plain, would give but a faint idea of the flurries and scurries of Wall Street bulls and bears in the midst of a round-up. When the market looks like going up, all hands are ready to lift it higher. When going down, all are ready to ride it to the bottom.

The result is, a succession of extremes; and even when the entire Exchange is not blindly swayed to one side or the other, nothing is more common among its operators than the formation of pools to advance particular stocks or of combinations to raid others, artificial agencies in both cases being freely used. How often, or rather how seldom, do Exchange quotations express the values that stocks would have if left to themselves or to the arbitrament of supply and demand!

In these things, as already said, to one familiar with Wall Street ways, there is nothing remarkable. It is upon fluctuations that stock speculation fattens. The delight of the regular Wall Street man is a wild market — the wilder the better. Quick changes bring him quick profits. He knows that a steady market means a dull market, and nothing does he more heartily detest. To him the most agreeable of all movements is that which sends up prices with a rush and a hurrah, creating what, in Wall Street parlance, is known as a “boom” and leading outsiders to purchase on the rise — of course, in the expectation of higher figures — and which then lets prices drop so suddenly as to shake or scare these purchasers out. In that way the broker gets both the money and the stocks, and the outsider gets a lesson.

It is the theory of experienced operators, and undoubtedly a correct one, that the outside speculator rarely comes into the market until prices are up, and he can look back and see what he has lost by not venturing earlier; and is never so ready to sell as when prices are down, and he can look back and see what he has lost by not getting out sooner.

Instead of being a balance-wheel to the business of the country, the Stock Exchange is far more likely to be a disturbing factor. It does not even furnish trustworthy news. Nowhere is it so difficult to get reliable intelligence concerning any stock dealt in there, as in Wall Street. The inventiveness of the speculative broker is something marvelous. He can ruin the country one hour and save it the next. He can blight the crops of a whole section, or he can fill the land with abundance. He can make war or he can make peace, exactly as his momentary interest demands. Rumor-mongering seems to be a part of his trade. He is the chief of liars. Perhaps he is the exception rather than the rule among his fellows — it is to be hoped that he is — but he is a pretty numerous exception, for all that!

What is the consequence? Simply that when a financial storm threatens the country, the Exchange is almost certain to be the center of disturbance. No other institution is so sensitive. It exaggerates all the symptoms of trouble. It sends out its alarming reports as the storm-cloud sends out its lightnings. Looking at it as the barometer of values, the timid naturally conclude that everything is lost, and thus the evil is unduly magnified. Wall Street is as much the natural field for panics as the prairie is for tornadoes.

If the Exchange has been of advantage to the business interests of the country, those who have had dealings with it should be ready to testify in its favor. Of the thousands and thousands who have visited it in person or by proxy, and done a little business with it, how many are ready to rise up and call it blessed, except in a very qualified sense? If all were to give their experiences, what would the verdict be? It is to be apprehended that the evidence of a very decided majority would not be flattering to Wall Street’s famous institution; that their testimony would be that they had found it easier to lose money there than to make it.

But why mince matters? Why deal in doubtful phrases? Why not at once declare what the discussion of the subject inevitably leads to — viz., that the New York Stock Exchange, which is the soul, the motive power of Wall Street, is an evil in the land, a danger to private wealth, a disturbing force in general business, and a foe to public morals. A not overdrawn description would picture it as an enormous devil-fish with a hundred thousand arms reaching into all parts of the country, and all equipped with suckers more or less powerful, and busy every one of them, in extracting nourishment for the monster to which it belongs.

The trouble is that its tentacles are rarely seen. They work in the dark; they have the gift of invisibility. But, oh, how many victims they have crushed! Yonder is a bank that is supposed to be as solid as the hills. Rich and poor make it the depository of their surpluses. It enjoys the confidence of all. But in an evil hour one of the arms of the Wall Street octopus has fastened itself upon it and penetrated to its safe, and pretty soon its president, or its cashier, or its managing director, will be gone — gone to Canada — and the bank will be wrecked. There is a citizen who has the respect of all. He is a good man, useful in his community, and the stronghold of his family and his friends. But, somehow, he is caught in the deadly embrace, and soon he will be a bankrupt and a defaulter, if not a suicide.

Such cases, by their frequency, have almost ceased to surprise; and yet they represent but a small portion of the losses actually wrought. Most of the injuries inflicted by stock-gambling are unknown, except to the sufferers. Wall Street’s victims, as a rule, do not expose their wounds unless they are mortal. The aggregate tax upon the country for the support of its operations is something enormous. It can not be otherwise when we see how Wall Street lives and flourishes. It maintains a good-sized army of operators, the membership of the Stock Exchange numbering nearly twelve hundred — without counting “curbstone ” men and other camp-followers — who spend with the lavishness of soldiers of fortune, while some of them take unparalleled fortunes out of the street.

And yet Wall Street does not produce a dollar. It creates nothing. It draws its sustenance entirely from outsiders. It is a blood-sucker. That Wall Street should continue to attract fresh patrons and victims, in view of the numerous warnings they have received, would be unaccountable were it not for that feverish desire for sudden riches which pervades the whole country, and which “the street” has been mainly instrumental in producing. It is said of the cuttle-fish that it discharges a fluid which darkens the water all about it, and so blinds its prey that they are helpless against its attacks. The Wall Street monster — the comparison still holds good — by the example of its few conspicuous successes and its general demoralization, so impregnates the atmosphere of the whole country with the speculative mania, that thousands and thousands can not resist it.

There is no village so small or so remote that it may not have its local speculator. No calling or profession escapes the contagion. The accommodations for all are ample. Wall Street has its wire connections with all points, and there are plenty of middle-men to instruct the uninitiated and take their orders for stocks. The “margin ” feature is the cleverest bait. The fact that, by putting up one thousand dollars in cash, you can buy or sell from ten to twenty thousand dollars in stocks, and take a profit on the larger amount, is to many an irresistible temptation.

Then, in theory, it is so easy to win by speculation! To buy at a low figure and sell at a higher, or to sell at a high figure and afterward buy at a lower, seems such a simple operation! It almost looks as if you could go into Wall Street and pick up money from the side-walks. Those who have made the attempt, however, have found the practice very different from the theory. When the cleverest operators, the trained habitués of the street, so often make shipwreck, what hope is there for the inexperienced?

A loss, however, is usually incurred beforethe real difficulties of the situation are realized, and then, in nine cases in ten, there exists on the part of speculators, out of sheer desperation or from the fascination that attends the game, the determination to try another chance, and in that way good money is thrown after bad until ruin is reached.

It is folly to charge upon Wall Street sharpers the seduction of such men. They lose because they want to make money, are not particular how they make it, and flatter themselves that they are sharp enough to win where others have failed. They are their own victims. And yet they are not the only sufferers, and possibly not the greatest. The man who wins somebody else’s money in Wall Street is far more than likely to lose it, and more with it, at the next venture he makes.

And even the few so-called lucky ones who retire with their winnings, are not under all circumstances to be envied. The triumph of the man who victimizes the public with watered stocks, which are no better than adulterated wares or counterfeited coin, is not without alloy. He may rejoice in the money, and in the fleeting importance it gives him, but he knows how he got his wealth, and he knows that others know how he got it. The sensitiveness of pride remains, even if conscience be dead.

But while the writer does not hesitate to arraign the New York Exchange, being the acknowledged center of stock speculation in the country, as an enemy to public morals and general business, he admits that it is not the only culprit of the kind. The Produce Exchange — or Board of Trade, as it is called — of Chicago, is a den of speculators, whose operations are even more pernicious. They affect more far-reaching interests. Stocks and bonds are in comparatively few hands, and these are generally strong enough to withstand ordinary fluctuations. But the produce-gambler deals with men’s necessities, he juggles with the staff of life. The soil-worker, who takes no part in the gamester’s operations, and is in no wise responsible for them, is liable at any time to be robbed of his just rewards through their deals and pools; and the mechanic or other wage-earner, who is equally innocent of complicity with them, is compelled to pay them tribute on every loaf of bread and every cut of beef or pork he puts into his own or his children’s mouths. Of all kinds of speculative gambling, that in breadstuffs and meats is the lowest, the meanest. The same comment, differing in degree only, will apply to such institutions as the Petroleum Board of Pittsburg. Indeed, it runs the whole gamut of the speculative “exchanges” and “boards,” from the highest down to the petit-larceny bucket-shop where, with a ten-dollar bill, you can purchase a chance on stocks, or oil, or wheat, or pork, or anything else that men gamble in. All are members of one family, and should be regarded and treated alike.

APPENDIX. INVESTMENT SECURITIES.

Any one having a negotiable security is naturally anxious to know its market value; especially so if looking for a purchaser. If the security happens to be listed at a stock-exchange, it is an easy matter to get a quotation on it, and a buyer can generally be found at some price. Or, if looking for a not very common security, any one may possibly be aided in his search by reference to the same quarter. Few, however, outside of professional bond and share dealers, are familiar with the transactions of the exchanges, and it is probable that a preponderance of the securities dealt in at their boards are in the hands of people ignorant of the positions they occupy. To such parties, as well as to those who may be in quest of particular bonds or shares, without knowing exactly where to look for them, and what their acquisition will cost, the following transcripts from the books of our principal exchanges, and showing the range of their operations, will be of interest, and sometimes of advantage. It will be seen that, beyond giving, to some extent, a preference to obligations that happen to be strictly local or most generally held in the neighborhood, no positive rule of selection has been observed in making up the lists. The good and the bad are mingled in a way that is quite indiscriminate, and which to the casual observer must be somewhat bewildering. To any one, however, who has read the accompanying chapters there will be no particular mystery about it. Indeed, it is partly to illustrate the points therein made that the following record is given. As prices bid or paid are constantly fluctuating, there is no use in giving present or recent figures; but any one interested in any of the securities on the lists can easily inform himself by applying to the proper quarter or quarters.

Read the rest of the column

This article was originally published on The Wall Street Journal.

Further reading

Benjamin Graham, The Intelligent Investor

Jason Zweig, The Devil’s Financial Dictionary

Jason Zweig, Your Money and Your Brain

Jason Zweig, The Little Book of Safe Money

Why Bankers Should Be Grateful for Occupy Wall Street

Trust: Easy to Break, Hard to Repair

Will We Ever Again Trust Wall Street?