From my archives, here’s the first of several articles I’ve written on the crepuscular practice of “window-dressing,” also called “painting the tape” or “leaning for the tape.” As the end of a month, quarter, or year approaches, portfolio managers can amplify their returns by aggressively buying a few more shares of stocks they already own. It’s hard to detect and extraordinarily hard to prove. Whenever I’ve asked portfolio managers about it, they always say something along the lines of, “Well, we don’t do it, but everybody else does.” What’s more, a fund manager can argue — perhaps even truthfully — that he bought the stock merely because it was cheap, and it just so happened to be especially cheap around 3:59 p.m. on Dec. 31, moments before the market closed for the year.

This particular article, I’ve been told, led the Securities and Exchange Commission to investigate the practice, resulting in at least one enforcement action. Two decades later, I believe year-end window-dressing has become quite rare, but I’d also be surprised if some fund managers didn’t still think they could get away with it.

Watch Out for the Year-end Fund Flimflam

If you think a fund’s annual return tell you much, think again. In an exclusive study, Money has found that many market-beating funds earn a big part of their annual results in one day.

Money Magazine, November 1997

What a difference a day makes!

With the end of the year approaching, it’s time for me to remind you, as emphatically as I can, that mutual fund performance numbers often don’t mean what you think they do — and short-term records may mean almost nothing. Consider this fact: A fund’s “annual” return can be completely distorted by how the fund performed on one single day. Indeed, as I’ll demonstrate in a moment, one day’s returns can often transform a market-lagging fund into a market beater for the entire calendar year. What’s more, for reasons that raise troubling questions about the ways some fund managers may operate, these one-day wonders often save their best day for last, sprinting past the market on the final trading day of the year.

Why should you care? If, like many people, you use calendar-year returns to help you pick funds, you’re using a flawed tool that may well prevent you from getting the solid performance you seek.

MONEY just completed an exclusive study that documents the New Year’s Eve effect (or what Wall Street has long called “window dressing”). The research was conducted for us by Mark Carhart, an assistant professor of finance at the Marshall Business School at the University of Southern California, based on comprehensive data provided by Micropal Inc. We looked at 1,550 diversified U.S. stock funds from 1985 through 1995. Here’s what we found:

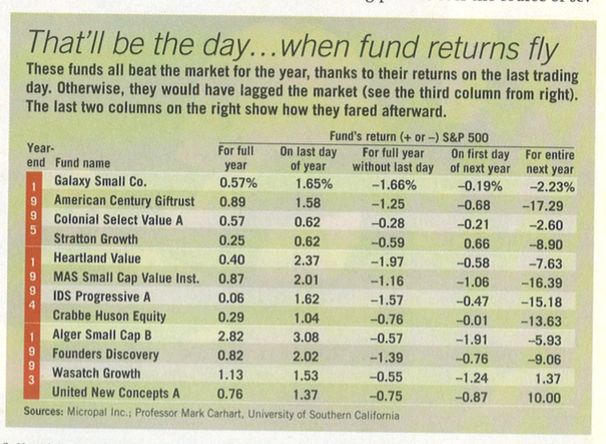

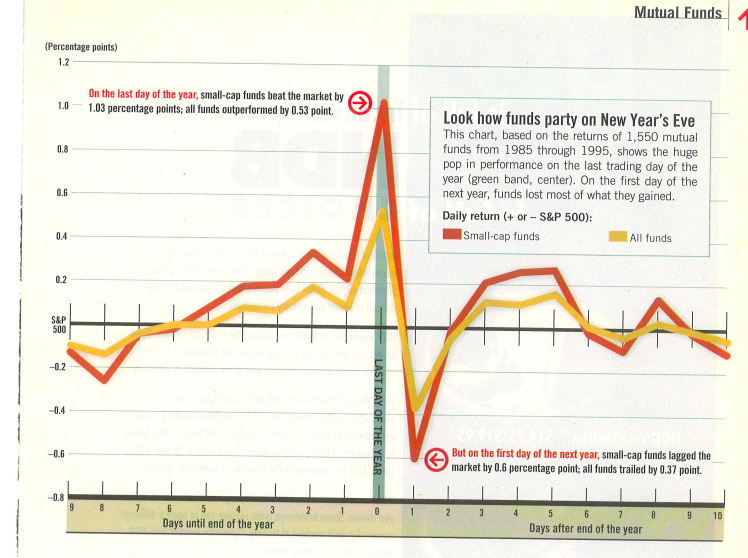

Funds clobber the market on the last day of the year. Look at the chart on the facing page. As you can see, on the last trading day of the year, the average fund beat Standard & Poor’s 500-stock index by 0.53 percentage point, and funds specializing in small stocks beat the market by an eye-popping 1.03 percentage points.

One great day can make a whole year look good. Let’s consider Alger Small Cap B. In 1993, this fund was 0.57 percentage point behind the market at the close of business on Dec. 30. But on Dec. 31, the year’s final trading day, Alger Small Cap beat the market by 3.08 points — transforming the fund, literally overnight, from a market loser to a market beater. Thanks to that single day, it beat the S&P 500 for the entire year by 2.82 percentage points — a record that brokers promptly trumpeted, raking $30 million into the $290 million fund over the next three months.

Nipping the market at the wire is no big deal. Among the 54 funds Carhart studied that were lagging the market by 0.1 percentage point or less as of the year’s next-to-last day, 69% went on to beat the market thanks to their returns on the year’s final day. Among the 143 funds that were behind by as much as 0.25 point, 62% nudged past the market for the entire year based just on the last day. Even among those that were behind by as much as half a point, 49% beat the S&P 500 for the entire year thanks to their last-day returns alone. Carhart’s 11-year analysis shows that it’s a cinch for a fund to beat the market for the whole year if it’s trailing by only a small amount going into the final day.

So how do so many funds get this final-day surge? “The funds appear to be ‘gaming’ the market,” says Carhart (meaning that they are creating an artificial performance edge, which I’ll explain shortly). Moreover, he says, the edge “isn’t sustainable for long.” In fact, as the chart above shows, on the first day of the following year, the average fund loses virtually all the extra return it picked up on New Year’s Eve. As you can see, the New Year’s Eve boost lasts about as long as a dusting of snow in early November.

If funds, on average, persistently fail to beat the market for most years, then how can they possibly beat it so badly on a single day? There are several possibilities, which I’ll list in order from most innocent to most sinister:

Small stocks party on New Year’s Eve. Carhart found that small stocks outpace the big companies in the S&P 500 by about one percentage point on the last day of the year. Since mutual funds tend to contain more small stocks than the market as a whole does, the funds benefit from this one-day blip in little stocks. Therefore, your fund manager’s “outperformance” may not only be coming just in a single day but also merely because he owns small stocks on the right day. That may not be skill at all; it might be luck.

Funds are neat freaks. Consultant Geoffrey Bobroff says that managers prefer round numbers. “Some fund executives feel that 122,000 shares of a stock ‘looks better’ than, say, 121,873 shares in the fund’s year-end report,” he says. “So they will round up many of their stock positions to even numbers. It’s a kind of housekeeping, but buying more of the stocks you already own can make them go up.” Buying even a few hundred shares of a rarely traded small stock can make the price rise — increasing the value not just of the new shares but also of all the fund’s existing stake in the same stock. And that in turn can make the whole fund’s performance move up.

Cash is trash. “If you show too much cash in your year-end report,” says Alger Small Cap manager David Alger, “some investors will complain, ‘If you’re bullish, then why do you have 10% in cash?’” Thus many fund managers take any spare cash and use it to buy stocks on the final day of the year. Since managers tend to buy more of the stocks they already own, that helps improve fund returns on the last day.

Funds are flooring it at the finish line. Now we’re getting into the less innocent possibilities. Mutual fund operators — along with other big market players like hedge funds — have an incentive to boost returns at year-end. Here’s why: A 1995 study by finance professors Erik Sirri and Peter Tufano found that the assets of the best-performing funds in a given year grow more than five times faster in the following year than those of the average fund. And that means more management fees — and heftier profits — for the company that runs the fund. Thus it would be no surprise if a fund manager chose to crank up his performance on the last day of the year.

“I think your hypothesis makes good sense,” Barry Barbash, chief fund regulator at the Securities and Exchange Commission, told me. “Fund managers are a lot like baseball players, trying to pad their performance numbers at the end of the season to get better contracts for the next year.”

There are two easy ways a fund manager can inflate his final-day returns: Buy call options, or derivatives that will surge in value if his most volatile stocks rise, or simply buy more of the small stocks he already owns, thus driving up the price of his new and old shares alike. Says Wayne Wagner, president of Plexus Group, a Los Angeles-based consultant on trading costs: “If you want a small stock to close up in price, you just need to make sure there’s a buyer at the end of the day — even if it’s you.”

If a fund manager deliberately did either of these things to manipulate his short-term performance, that would be illegal — but the SEC would have to prove that the manager’s actions were deliberate, which is tough to do. Explains Barbash: “We have seen, during the course of our inspections of funds, evidence that some managers engaged in a transaction to manipulate performance at year-end.” For example, he says, a fund group that almost never used options traded heavily in them on the last day of the year. “But,” he adds ruefully, “it’s extremely difficult for us to show that the manager intended to manipulate the returns. He can simply say, ‘I liked the stock.’”

Indeed, I got in touch with nearly a dozen fund managers for this article, and each one said he hadn’t a clue why his fund fared so well on the last day of a given year. “It’s a mystery to me,” says Alger. “There are a lot of people who play the window-dressing game,” says Richard Huson of Crabbe Huson Equity Fund, “but we don’t.” Robert Puff, chief investment officer of the American Century funds, “has no idea” why some of the firm’s funds do so well on the last day of the year, says a company spokesman. Several managers speculate that risk-loving hedge funds might be bidding up small stocks also owned in mutual fund portfolios, lifting their values as well.

Fair enough. But the stark fact stands: Over the period we studied, 90% of the 1,550 funds beat the market on the last day of the year at least once. The sad truth is that it’s impossible for any outsider to know for sure which funds are gaming the system and which are benefiting from someone else’s flimflam.

So what should you do about all this?

Don’t be a sucker for short-term performance. As I’ve shown, many “annual” returns should really be called “daily” returns — but you can’t tell which unless you compare a fund’s results against the market day by day as the year comes to a close. “Because performance is expressed as an exact number,” says fund cop Barbash, “it’s easy to understand what the number is. But it’s hard to understand what it means.” Since calendar-year returns may well have been distorted in a single day, they’re not a long-term measure of performance, and you should not rely on them as your main analytical tool. You should also scan a fund’s returns over three, five and 10 years to help iron out any daily wrinkles.

Use rolling time periods. To supplement calendar-year returns, look at rolling one-year periods: the 12 months that ended in January, the 12 months that ended in February, and so forth, comparing a fund against the market and against similar funds for each of the rolling periods over the course of several years. Some fund companies may provide such data. Information is also available on Morningstar’s Principia Plus software ($495; 800-735-0700) and at Microsoft Investor (investor.msn.com) in the Research Central feature.

Consider index funds. Because index funds are simply computer-guided replicas of the market’s performance, their managers won’t play games to beat the market. You should always get the market’s return, minus the index fund’s expenses–no more and no less, without any year-end hanky-panky.

Remember that “beating the market” isn’t the only thing that matters. If outperforming the market for the entire year is often just a 24-hour phenomenon, then you need to realize that beating the S&P 500 is not a very sound measure of success. Instead of worrying about whether each of your funds is beating the benchmark, you should concentrate on whether you’re on track to meet your goals. Sure, the market is up 28% so far this year — but should you really be angry at your fund manager if he’s up “only” 25%? Of course not — that’s still more than double the long-term annual average return of stocks. That “underperforming” manager has you well ahead of where history says you should normally be. So if you have a fund with a good long-term record that’s trailing the market by a tad, don’t sell it to buy another with better “annual” performance. You don’t want to end up with a fund that’s just a one-day wonder.

This chart, based on the returns of 1,550 mutual funds from 1985 through 1995, shows the huge pop in performance on the last trading day of the year (green band, center). On the first day of the next year, funds lost most of what they gained.

Additional resources:

Books

Definitions of MUTUAL FUND, PERFORMANCE, PORTFOLIO MANAGER, SHORT TERM in The Devil’s Financial Dictionary

Chapter Four, “Prediction,” in Your Money and Your Brain

Articles

{kind=link}

Fund Managers Lift Results with Timely Trading Sprees

‘Tis the Season for Window Dressing

Trust: Easy to Break, Hard to Repair

Will We Ever Again Trust Wall Street?

Saving Investors from Themselves

How Fast Should You Trade Your 401(k)?

Phishing for Phools: A Q&A with George Akerlof and Robert Shiller

Read the rest of the column

This article was originally published on The Wall Street Journal.