Here is the first article in which I explored in some detail the emerging science of neuroeconomics. It sprang originally from a column I’d written in November 2000. When I discussed that research with the psychologist Daniel Kahneman, he offhandedly mentioned that a conference on the topic would be held at the University of Arizona. I immediately signed up; there, I met several of the pioneering researchers in the field and was instantly hooked. For much of the next two years, I read constantly in the field, interviewed leading neuroscientists, and had my own brain scanned in numerous experiments. What I learned ultimately led to my book Your Money and Your Brain.

Are You Wired for Wealth?

What goes on inside your brain when you invest? Here’s how the latest breakthroughs in neuroscience can help make you smarter — and richer. Money Magazine, October 2002

With the bull market in ruins around us, many investors have never felt more bewildered. And they are asking agonized questions: How could I have lost so much money so fast? Can I do better somehow? Will I ever make money in the market again?

You won’t find the answers by beating yourself up over the mistakes you’ve made in the past few years. No matter how many times you kick yourself for having been so stupid, your investment IQ is not going to budge. But there is a totally new and profoundly effective way to become a smarter investor.

Suddenly, stunning investment insights are coming from the frontiers of one of the least likely fields you could imagine: neuroscience. In university and hospital laboratories around the world, researchers are using the latest breakthroughs in technology to trace the exact circuitry your brain uses to make the kinds of decisions you rely on as an investor.

For the first time in any nonscientific publication, this article will take you deep inside your own brain to help you understand why you invest the way you do — and, more important, how to enhance the workings of your brain to get better results.

I think you’ll see that the neuroscience of investing helps explain one puzzle after another: why we chronically buy high and sell low, why “predictable” growth stocks sell at such high prices, why it’s so hard to understand our own risk tolerance until we lose money, why we keep buying IPOs and “hot funds” despite all the evidence that we shouldn’t, why stocks that miss earnings forecasts by a penny can lose billions of dollars of market value in seconds.

I’ve spent much of the past year studying this research — even having my own brain studied by these researchers — and nothing I’ve ever learned about investing has excited me more. Delving into the brain with MRI and other scanning techniques, scientists can now observe the mechanisms our brains use to reckon the value of rewards, interpret probabilities and estimate risks — the very essence of investing. These processes, says Jordan Grafman, a neuroscientist at the National Institutes of Health, “go right to the heart of who we are as humans.”

Fortunately, the latest discoveries also point the way toward cures for bad investing behavior. “Investors are human,” says Andrew Lo, a finance professor at the Massachusetts Institute of Technology. “Therefore, how the human brain works and why we react the way we do to various situations are critical for developing a better understanding of the common mistakes that typical investors make.”

How We Got Our Brains

For nearly our entire history as a species, humans were hunter-gatherers, living in small nomadic bands, pursuing wild animals, foraging for edible plants, finding mates, avoiding predators, seeking shelter in bad weather. Those are the tasks our brains evolved to perform.

In the formative dawn of human history, someone who kept failing to predict where food could be found would have starved to death, while anyone who correctly gambled on finding an unlikely cache of food would have been a hero. Meanwhile, someone who underestimated a risk would have become a quick snack for a wild carnivore.

Our modern skulls house a Stone Age mind, evolutionary psychologists Leda Cosmides and John Tooby have written. The human brain is a superb machine — “a Maserati,” says Baylor College of Medicine neuroscientist Read Montague — when it comes to solving ancient problems like recognizing short-term trends or generating emotional responses with lightning speed. But it’s not so good at discerning long-term patterns or focusing on many factors at once — challenges that our early ancestors rarely faced but that we investors confront every day.

The Kernel of Emotion

Now let’s take a tour of your investing brain. Our first stop is the amygdala (a-MIG-duh-luh), deep in the forward lower area of the brain. (There’s one on the left side and one on the right.)

A key part of your brain’s early warning system, the almond-shaped amygdala is a kernel of hot, fast emotions like fear and anger. If I threw a rattlesnake in your lap, you wouldn’t ruminate about whether it was real or a rubber toy. You’d go flying out of your chair. That’s the amygdala kicking in.

Vivid sights and sounds, such as clanging bells, hollering voices and waving arms, can set off the amygdala. Before you even figure out what the fuss is about, you break out in a sweat, your breathing picks up, your heart races. This primal part of your brain is bracing you for a “fight or flight” response.

And it isn’t only the threat of physical danger that sets off the amygdala. Using MRI scans, neuroscientists have found that financial gains have a fairly strong effect on the amygdala — and losses make it flare up like a hot coal.

One recent study, led by Grafman of the NIH, found that the more frequently people were told they were losing money, the more active their amygdalas became.

And a team of researchers led by Hans Breiter of Harvard found last year that even the expectation of losses sets off a burst of activity in the amygdala.

Long ago, on the plains of the Serengeti, there was probably no harm in confusing false alarms and real ones. If your amygdala sent you scrambling up a tree to escape a lion, you were safe; if what seemed like a lion turned out to be only a patch of brown grass rippling in the wind, having climbed up that tree did you no harm.

But in the world of investing, a panicky response to a false alarm — dumping all your stocks just because the Dow is dropping — can be as costly as ignoring real danger. For one thing, it can cause you to flee the market at a low point and miss out when the market bounces back.

A moment of panic can also disrupt your long-term investing strategy. Activity in the amygdala can trigger the release of adrenaline, which has been found to “fuse” memories, making them more indelible.

Research by Raymond Dolan of England’s University College London has also shown that a financial losing streak heats up activation of the hippocampus, a part of the brain next to the amygdala that helps program our memories of fear and anxiety. That may help explain why market crashes, which make stocks cheaper to buy, also make investors less willing to buy them for a long time to come.

No Pain, No Gain

But the hot emotions triggered by the amygdala can be beneficial, too — as I learned in April, when I participated in an experiment at the University of Iowa.

First I was wired up with roughly a dozen electrodes and other monitoring gizmos — on my chest, my palms, my face — to track my breathing, heartbeat and perspiration. Then I played a computer game designed by neurologist Antoine Bechara. Starting with $2,000 in play money, I clicked a mouse to select a card from one of four decks on the monitor of a Dell PC. Each “draw” made me either “richer” or “poorer.”

I soon learned that the two left decks were more likely to produce big gains and even bigger losses, while the two right-hand decks combined smaller, more frequent gains with a lower chance of big losses. Gradually, I began picking all my cards from the right.

After the experiment, I looked over the printout of my bodily responses: At first, my skin would sweat, my breath quicken, my heart race and my facial muscles furrow immediately after I clicked on any card that cost me money. When I drew one card that lost me more than $1,100, my pulse shot from 75 to 140 in a split second.

After I had suffered three or four bad losses from the riskier decks, my bodily responses surged whenever I even considered selecting a card from one of those two piles.

In a matter of minutes, my amygdala had already created an emotional memory that made my body tingle with apprehension at the very thought of taking a big risk — even with play money.

Ironically, then, this highly “emotional” part of our brain can help make us more rational. Bechara’s experiments show that people with damaged amygdalas never learn to avoid picking from the riskier decks. Since their amygdalas can no longer signal how painful it will feel to lose money, their prefrontal cortex — the “thinking” part of the brain — leads them to sample cards from all the decks until they go broke.

“The process of deciding advantageously is not just logical but also emotional,” concludes Antonio Damasio, chief of neurology at the University of Iowa.

Ignoring that biological fact can cost you a fortune. During the peak of the bull market, many investors bragged that they had a high tolerance for risk. Thanks to a streak of glorious gains in the late 1990s, these investors’ amygdalas had never been ignited by a major financial loss. That led all too many people to the mistaken conclusion that big losses wouldn’t bother them. But big financial losses are always painful to anyone with a normal brain, because our mental circuits respond so powerfully to any vivid danger.

Imagining that you can shrug off setbacks before you’ve ever suffered any is a disastrous illusion — since it leads you into taking such high risks that huge losses become inevitable.

The CEO of the Brain

If nothing could counter the fight-or-flight function of the amygdala, we might never have a moment’s peace. Fortunately, the prefrontal cortex, a region of the brain behind the forehead, allows us to store sets of events in the form of memories, to draw general conclusions from particular data, to forecast the consequences of our actions and to compare current and past experiences — thus helping us reach more balanced judgments. Grafman of the NIH calls the prefrontal cortex “the CEO of the brain.” (He means that it makes executive decisions, not that it’s corrupt.)

Grafman studied a group of Vietnam war veterans who had been injured in the prefrontal cortex. He found that the further off a financial goal was, the less planning these patients were capable of devoting to it.

Grafman’s experiments showed that people with cortex damage pay even more attention than normal people do to short-term goals like stabilizing their income or paying for a house within the next two years. But the injured veterans spent less than half the normal time on planning to pay for their children’s college education — and virtually no time at all on making financial plans for retirement.

Antoine Bechara points out that various forms of dementia (age-related declines in mental sharpness) can begin in the prefrontal cortex. That may explain why the elderly disproportionately fall prey to investing scams. With their planning abilities impaired, they can fail to understand the future consequences of financial decisions.

“Scams often offer the prospect of immediate rewards,” says Bechara. “You can only resist that temptation if you can keep the long-term consequences in mind. Even slight damage to this part of the brain can cause a myopia for the future.”

The Prediction Addiction

If you show people a sequence of anything — numbers, colors, shapes, letters, faces — and tell them that the arrangement is random, they will insist on believing that they can predict the next item in the series. Examples are everywhere: We “know” that a baseball player is “due” for a base hit, we’re “sure” that our next roll of the dice will be a seven, we can tell that our “lucky number” will be the winner in this week’s lottery.

Technical analysts insist that charts of past prices can predict the path of future returns — and every Wall Street strategist thinks he can forecast where the market is headed, especially when you seat him in front of a TV camera.

At heart, all of us (even market strategists) know that these things are utterly unpredictable. So why do we persist in trying to predict them?

It turns out that we have no choice. Our brains are wired to force us into forecasting; it is a biological imperative. In fact, humans are born with what I’ve come to call “the prediction addiction.”

Two areas of your brain, the nucleus accumbens and the anterior cingulate, specialize in recognizing patterns and choosing between conflicting alternatives.

The nucleus accumbens lies on the bottom surface of the front of your brain; the anterior cingulate is in the central frontal area.

These areas click into life when the stimuli around you either repeat or alternate. Repetition (this plant always has edible roots) and alternation (day always follows night) were the two most basic patterns primitive man had to recognize. After millions of years of evolution, our brains now respond to these simple patterns unconsciously, automatically and involuntarily.

You don’t even realize that you’re searching for patterns — and you can’t stop it, any more than you can order your heart to cease beating or your lungs to shut down.

What’s more, these two parts of your brain (along with other, interconnected structures) pounce on patterns almost instantly. Scott Huettel, a neuroscientist at Duke University, recently found that the anterior cingulate begins to anticipate another repetition after a stimulus occurs only twice in a row. (There’s neural truth in the old saying, “Three’s a trend.”)

In other words, as soon as a stock beats earnings forecasts for two consecutive quarters, or a fund outperforms the market for two straight years, an “I get it” effect kicks in — the conviction that you know what’s coming next.

But Huettel’s experiments show that there’s a dark side to this trait. If a repeating pattern is broken (as it so often is in the financial markets), then batches of neurons suddenly flare in the insula, caudate and putamen — areas of the inner brain that, like the amygdala, can generate feelings of fear and anxiety.

That may help explain why, when the earnings of “predictable” growth companies stop growing, investors bail out and these stocks can lose billions of dollars in market value in a matter of moments.

Huettel also found that the longer a pattern has previously repeated, the more violently your brain responds when the pattern is broken.

The stock market bears out Huettel’s laboratory findings: A recent study by Irene Kim, a finance scholar at the University of Michigan, shows that the more times in a row a company has topped Wall Street’s expectations, the further its stock drops when it finally falls short of analyst forecasts.

While a shortfall after a run of three good earnings reports trims just 3 percent off the price of the average growth stock, a miss after a string of eight positive quarters hacks off an average of 8 percent. (One recent example: In July, after eight straight quarters of “beating the Street,” NCR Corp. earned one penny less than expected — and lost 15 percent of its value in a day.)

And what about value investing? Value stocks tend to have lumpier, less linear earnings; as their profits and share prices bounce around, our brains probably seek to interpret them as an alternating pattern. But alternation is hard for us to grasp. Huettel has shown that the anterior cingulate takes much longer to “make a representation” of an alternating pattern than a repeating one — about six iterations, as opposed to two.

That may show why value stocks are so consistently underpriced: Because the path of their earnings growth is more erratic in the short run, your anterior cingulate struggles harder to predict what’s coming next.

In fact, that short-term focus of our brains leads us to overlook the longer-term truth: Over the course of many years, the earnings growth rate of value stocks is barely lower than that of their growth counterparts and, in the long run, value investing is at least as lucrative as a growth-only strategy.

Why Do You Think They Call It Dopamine?

Wolfram Schultz, a neurophysiologist at the University of Cambridge in England, is so fastidious that he turns his office teacups upside-down on a towel when he’s not using them, lest they get dusty. Schultz has the right temperament for someone who explores the microstructure of the brain, monitoring the electrochemical activity of one neuron at a time.

Schultz studies the workings of dopamine, the brain chemical that gives you a “natural high.” Dopamine is what makes you feel good when a stock you buy goes up, and neurons transmit that chemical to many parts of the brain, including the nucleus accumbens.

The latest scientific discoveries about dopamine have huge implications for investing.

First, your brain loves long shots. The less likely or predictable a reward is, the more active your dopamine neurons become and the longer they fire — flooding your brain with a soft euphoria.

“That positive reinforcement,” says Schultz, “creates a special kind of attention dedicated to rewards. Rewards are what keep you coming back for more.”

That release of dopamine after an unexpected reward makes humans willing to take risks. Without it, explains Baylor’s Read Montague, our early ancestors might have starved to death cowering in caves, and we modern investors would keep all our money under our mattresses.

The dopamine rush we get from long shots is why we play lotto, invest in IPOs, keep too much money in too few stocks and invest with active portfolio managers instead of index funds. It’s why phrases like “the next Microsoft” or “the next Peter Lynch” make us whip out our wallets.

Even if you’ve never experienced such a big score, you’re wired to want them. Dopamine makes winning big feel vastly better than just winning — and the prospect of its euphoric effect prevents us from focusing on how small the odds of winning big actually are.

The second dopamine discovery is reminiscent of Pavlov’s dogs. Russian physiologist Ivan Pavlov would ring a bell whenever his laboratory dogs were to be fed. After a while, they would drool at the mere sound of the bell, before the food even arrived. Dopamine works in a similar way. Once a gain becomes associated with a particular cue, your brain releases dopamine on that cue — before the gain occurs.

A team led by Harvard’s Hans Breiter found a “striking” similarity between the brains of people trying to predict financial rewards and the brains of cocaine addicts and morphine users.

In effect, as investors, we get stoned on our own belief that we know what’s coming. As time passes, we may get more of a dopamine high from predicting a coming gain than from earning the gain itself.

Thus, back in the booming bull market of 1999, day-traders got a “buzz” just from sitting down in front of their computers if their previous trades had been profitable. (That dopamine buzz probably made their next trades even more aggressive.)

And when Cisco had beaten Wall Street’s earnings forecasts for 25 quarters in a row, just the approach of its next earnings announcement made investors feel euphoric. (Perhaps that’s why Cisco’s price/earnings ratio hit an electrifying 196 times earnings by early 2000.)

The third major dopamine finding: Once you’ve learned which cues seem to predict a coming gain, something strange happens if that reward fails to materialize. Your neurons still flood your brain with dopamine when you encounter the cue, giving you that “prediction high.” But your dopamine dries up instantly if the gain fails to arrive when the cue suggested it would.

It’s as if someone yanked away the needle just as an addict was about to get his fix. This wrenching swing from euphoria to depression — which can take place in less than two seconds — may help explain why the market overreacts so harshly to any short-term disappointment.

Drinking the Kool-Aid

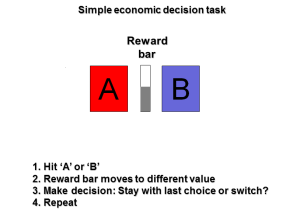

I came face-to-face with the workings of my own brain twice recently. First, in April, I saw my amygdala in action (see above). Then, in July, dopamine research pioneer Read Montague and leading neuropsychiatrist Gregory Berns of Emory University put me through an MRI scanner at Emory’s medical school in Atlanta.

Although I was mostly immobilized inside the MRI tube, my index fingers were free to press a touchpad on either side of my body.

On a display area above my face, the scientists projected a simple experiment: I could choose a red square, on the left, by pressing my left index finger, or a blue square, on the right, with my right index finger.

A slider bar between the boxes rose and fell to show whether my choice was a winner or a loser. The objective was to drive the slider up, earning the maximum of $40.

Meanwhile, the magnetic field of the MRI machine would trace the ebb and flow of blood inside my brain, creating a map of my neural “hot spots” as I thought my way through the experiment.

But there was one catch. As I lay in the MRI tube, I was sucking on a baby pacifier. No, I didn’t miss my mommy: It was part of the experiment. As I picked either the left or right box, trying to figure out which one (or which combination of them) would earn me the most money, little squirts of liquid trickled into my mouth through tubes hooked up to the pacifier. One tube squirted Kool-Aid (flavor: Tropical Fruit Burst). The other delivered plain water.

But the squirts did not come every time I pressed the buttons. The boxes were as irksomely random as the squirts were.

Picking the left box sometimes gave me a gain, sometimes a loss; same with the right box; same with two in a row for either box, or three in a row, or any other combination I could string together.

It was frustrating, almost maddening: No matter how hard I tried, I couldn’t figure out which box to pick next, and the slider bar on my overhead display just kept jitterbugging up and down around the midpoint, instead of rising toward the jackpot.

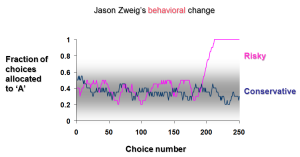

And then, suddenly, as I watched in wonder, my slider bar shot straight up.

With a shock of recognition, I realized that my left index finger had been clicking madly while my right hand had lain still.

And then I noticed that my mouth was full of Kool-Aid.

What on earth was going on?

Quite simply, the unconscious part of my brain had figured out the pattern before the “thinking” part could.

Although the squirts had seemed random, I got water only when I picked the right box and Kool-Aid only when I picked the left. The pattern had seemed chaotic because, on average, the liquid was delivered only one-third of the time.

While I was struggling to figureout which sequence of choices would work best, my nucleus accumbens suddenly recognized that sweet liquid arrived only if I picked the left-hand box.

So, without the slightest idea I was doing it, I had begun picking the left square every time — the only response in this experiment, it turns out, that would move the slider up to hit the jackpot.

This instinctual recognition of patterns by the nucleus accumbens is what Berns calls “learning without awareness.”

Patterns, especially repetition, trigger a subconscious, automatic and uncontrollable response in this part of the brain. That appears to explain why, if a stock goes up a couple of days in a row, or a company reports improved earnings for a few straight quarters, we immediately think that we know what’s coming next. The nucleus accumbens just can’t help itself. Instead of reaching an objectively factual conclusion — “so far, this stock has been going up” — we inevitably tell ourselves something speculative: “This stock is going to keep going up.” All too often, that turns out to be wrong — but our brains are hardwired to project the past into the future.

Chain Your Brain

Finally, let’s think about how you can use these new insights into the brain to make yourself a better investor. “You will be much more in control,” says Antonio Damasio of the University of Iowa, “if you realize how much you are not in control.”

Damasio’s point is both simple and profound: Since it’s impossible to change how the brain works, you must learn to make the most of its strengths and limitations alike.

Whenever possible, you need to develop automated, irreversible investing habits that are tailor-made for neutralizing your brain’s worst liabilities while optimizing its greatest assets. Here’s how neuroscience leads to a new science of investing.

Strap yourself in. Because the amygdala is an almost irresistible force, you must reduce your exposure to images that can provoke panic. Turn away from stock tickers; turn off the televised images of closing bells and yelling traders. And promise aloud or in writing, before a friend or family member who can hold you to it, that you won’t check the value of your accounts more than once a month. If you haven’t already, sign yourself up to dollar-cost average through an automatic investment plan that will electronically purchase shares in a mutual fund every month. That way, your investing commitment can never flag, even when you are full of fear.

Stay in balance. Geniuses like Warren Buffett can get away with putting all their money in a handful of holdings. The rest of us need to set limits on our prediction addiction. Give your broker a limit order that will automatically sell any stock that grows to more than 10% of your total. And if your long-term goal is to have, say 75% of your assets in stocks, but they’ve shriveled to 49%, buy enough to get them back up to 75%. Make that kind of asset reallocation twice a year, every year — no more, no less — on equidistant, easily memorable dates like New Year’s Eve and July 4.

Redouble your research. If a stock or fund goes straight up, don’t just enjoy the ride. The better an investment does for you, the more powerfully your brain will believe nothing can ever go wrong with it. Each time it rises, say, 50 percent, study it again more closely; ask what could go wrong; seek out negative opinions. The time to do the most homework is before bad news can catch your brain by surprise. There are no guarantees, but doing extra research just when things are going well is the best way to prepare yourself in case something later goes wrong — or seems to. You’ll then have a better sense of whether it’s a false alarm or a real one.

Use different wallets. If you can’t stop chasing “the next Microsoft,” at least chase it with only part of your money. Just as prudent gamblers lock most of their cash in the hotel-room safe and go onto the casino floor with no more than they’re willing to lose, you should set up a “mad money” account. You can’t control your prediction addiction, but you can at least contain it — by putting into your mad-money account only what you can afford to lose. That way, you speculate with a fraction of your money, not with all of it.

Build an emotional registry. Remembering what you did is only one way to learn from your own experience. Emotions can be an excellent guide to what you should and shouldn’t do. But to use them as an accurate guide, you need to remind yourself of how you felt after your decisions (and their results).

“Regularly evaluating whether an outcome made you feel good or bad,” says University of Iowa’s Antoine Bechara, “will help you learn from your behavior.” Keeping a written record of your feelings — what Bechara calls an emotional registry — is a good idea, particularly if you are a younger investor. Store these “feeling records” alongside your trading records.

Look at the long run. Remember that your brain perceives anything that repeats a couple of times as a trend — so never buy a stock or a fund because its short-term returns look hot. Check out the long run, and never assess performance in isolation; always compare a stock or fund to other similar choices.

Flex your cortex. Because your prefrontal cortex is responsible for evaluating the consequences of your actions, and because advancing age impairs that part of your brain, be on guard. If you (or members of your family) are elderly, simple reminders can help — like a note next to the phone that says, “No thanks to telemarketers” or a Post-It note on your PC that reads, “Never open unsolicited investing e-mail.”

Diversify, diversify, diversify. This grim bear market has revealed the biggest risk of all: underestimating your own tolerance for risk. Thinking you can tough it out, then suddenly finding you can’t, is a recipe for financial disaster. Diversification — making sure that you never keep all your money in one kind of investment — is the single most powerful way to prevent your brain from working against you.

By always holding some cash, some bonds, some real estate, some U.S. and foreign stocks, you ensure that your prediction addiction can never force you into a single, sweeping bet on a “trend” that disappears. And by keeping your money in a broad basket of assets, you lower the odds that a meltdown in one investment will send your amygdala into overdrive.

Putting yourself on investing autopilot minimizes the opportunities for your brain to perceive trends that aren’t there, to overreact when apparent trends turn out to be illusions or to panic when fear is in the air. That frees up your brain to focus on the harder work of long-term financial planning.

Above all, you should take enormous comfort from knowing that the latest scientific findings show just how newly valid the oldest truths of investing really are.

Read the rest of the column

This article was originally published on The Wall Street Journal.

Further reading

Definitions of BEHAVIORAL ECONOMICS, BUBBLE, GAIN, IRRATIONAL, INVEST, LOSE, PAREIDOLIA, RISK, and SPECULATE in Jason Zweig, The Devil’s Financial Dictionary

Jason Zweig, Your Money and Your Brain

Antonio Damasio, Descartes’ Error: Emotion, Reason and the Human Brain

Paul W. Glimcher, Decisions, Uncertainty, and the Brain: The Science of Neuroeconomics

Read Montague, Why Choose This Book? How We Make Decisions

Colin Camerer et al., “Neuroeconomics: How Neuroscience Can Inform Economics“

George Loewenstein et al., “Neuroeconomics“

Brian Knutson, “Neuroeconomics and Emotion” (video at YaleCourses channel on YouTube)